Below are income multiples for publicly traded shopper tech firms (B2C). Industries and subsequently multiples range extensively. Commentary is beneath. If you’re on the lookout for knowledge on SaaS multiples, hold scrolling.

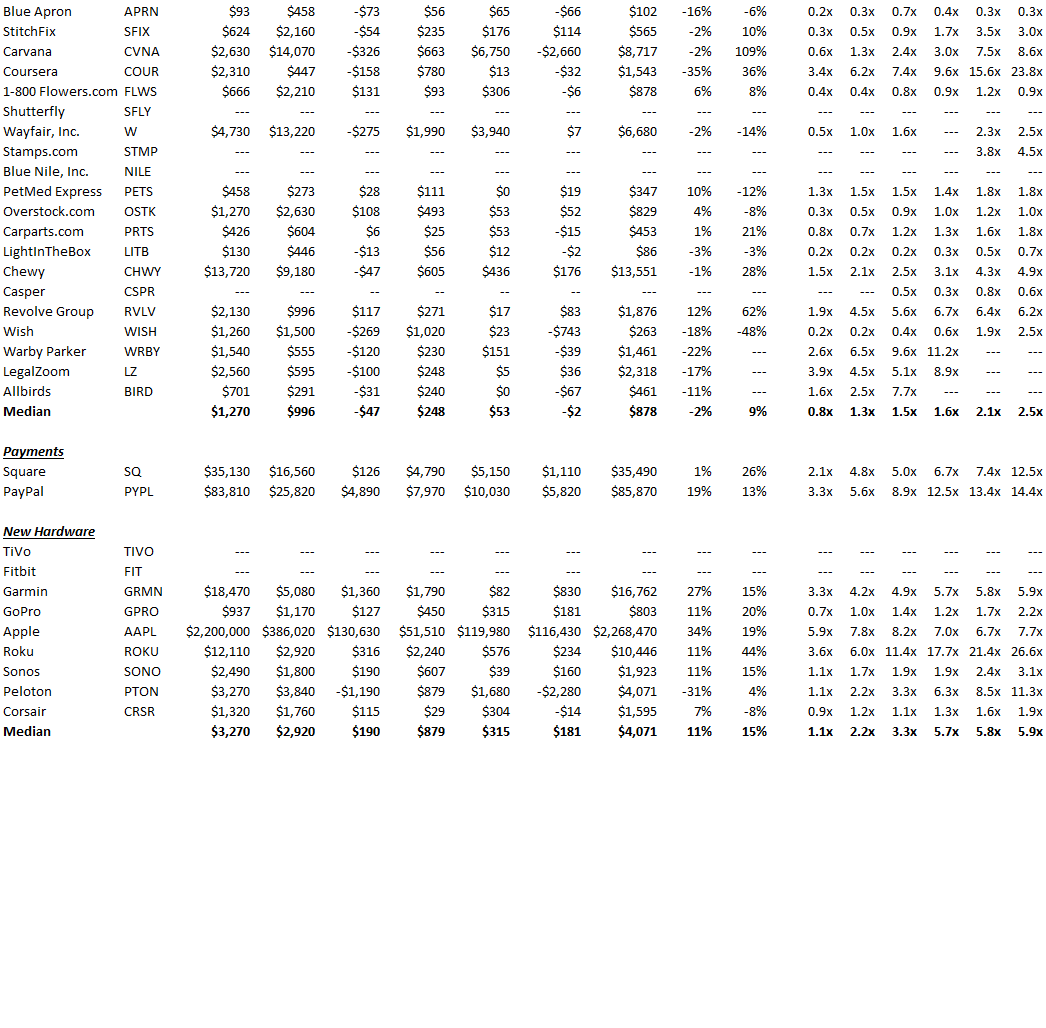

Social media is at an all-time low of 4.6x. Multiples rose steadily via 2020 peaking at 22.7x on median in Q1 2021. YOY progress within the area is improbable (36% on median), with Snap and Pinterest main the way in which. Facebook continues to be the monster within the area with $119bln of annual income and an outstanding EBITDA margin of 43%. The newcomer, Doximity, is buying and selling at 17x, which doesn’t appear sustainable relative to friends.

Travel marketplaces all the way down to 2.8x. Multiples hit 10.6x in Q2 2021 which is outstanding for a enterprise that historically trades no higher than ~3x. Booking.com is buying and selling at 6.3x.

Traditional market multiples range extensively. Prior to Q3 2018, the sector solely had 2 firms and now has 11. The median a number of is now 2.6x, however Etsy, Fiverr, Upwork and AirBnB have stronger multiples. eBay has the very best margin at 32%, whereas Airbnb combines good progress (93%) and a revenue margin of 13%.

Labor intensive area. The solely purpose we even embrace these firms in our evaluation is as a result of traders like Softbank insist on labelling these providers companies as tech co’s. At greatest, they’re tech enabled which isn’t the identical factor in any respect. Remember when Groupon was a excessive flier? Well as we speak it’s shrinking (-35% YOY progress) and trades at 0.5x income. Cash on the books represents almost your entire the market cap. This was one of many quickest rising firms ever that got here up in the course of the recession of ’08, and now nobody cares. Redfin and Opendoor have been decimated over time. OpenDoor, Redfin, and Compass don’t earn money, which is a really harmful place to be for providers companies of their measurement.

Other Outliers. DraftKings trades at 3.5x, manner down from it’s 47x days. DoorDash trades at 3.6x, down from 22.3x. Robinhood really has detrimental enterprise worth (money exceeds market cap and debt).

Rideshare multiples crushed. Lyft is at 1.1x income whereas Uber is at 2.3x income. We suspect the income a number of for each could be larger, however each companies gentle money on fireplace. Lyft’s EBITDA margin is -20% and Uber’s is -9%. It’s onerous to examine both firm producing money any time within the close to future given their present market share and really excessive ranges of burn, and take into accout meals supply saved Uber throughout 2020. Bird is buying and selling at 0.8x as their enterprise mannequin is damaged and so they appear headed to insolvency.

Subscription. B2C subscription is a wonderful enterprise mannequin however now trades at 3.8x income. Match could also be the very best enterprise mannequin, with 31% margins and 24% YOYG. Duolingo which is latest to the group trades at 12.0x.

Gaming. The median income a number of of 5.3x is robust. SciPlay is a multitude whereas Roblox cratered to 14x from a excessive of 42x. In 2021 Roblox received hit with a $200mm lawsuit over music rights (June 2021).

Ecommerce is assorted. The sector is the least enticing to traders, with a median income a number of of 0.8x. There is a giant distinction between what we’d name premium ecommerce like Carvana, Allbirds, Coursera, Chewy, Warby, LegalZoom, and Amazon, versus weak ecommerce like Blue Apron (0.2x income). Note that the margins in ecommerce are horrible with a median EBITDA margin of -2%. Amazon is at 12%, however $14bln of their $23bln of 2020 working revenue (61%) got here from AWS, whereas AWS was $45bln of their $386bln of web gross sales in 2020 (12%).

Hardware is all the way down to 1.1x. Roku has fallen probably the most. Apple’s progress is nineteen%, very sturdy for a corporation with $386bln in annual gross sales and a 34% margin.

SaaS

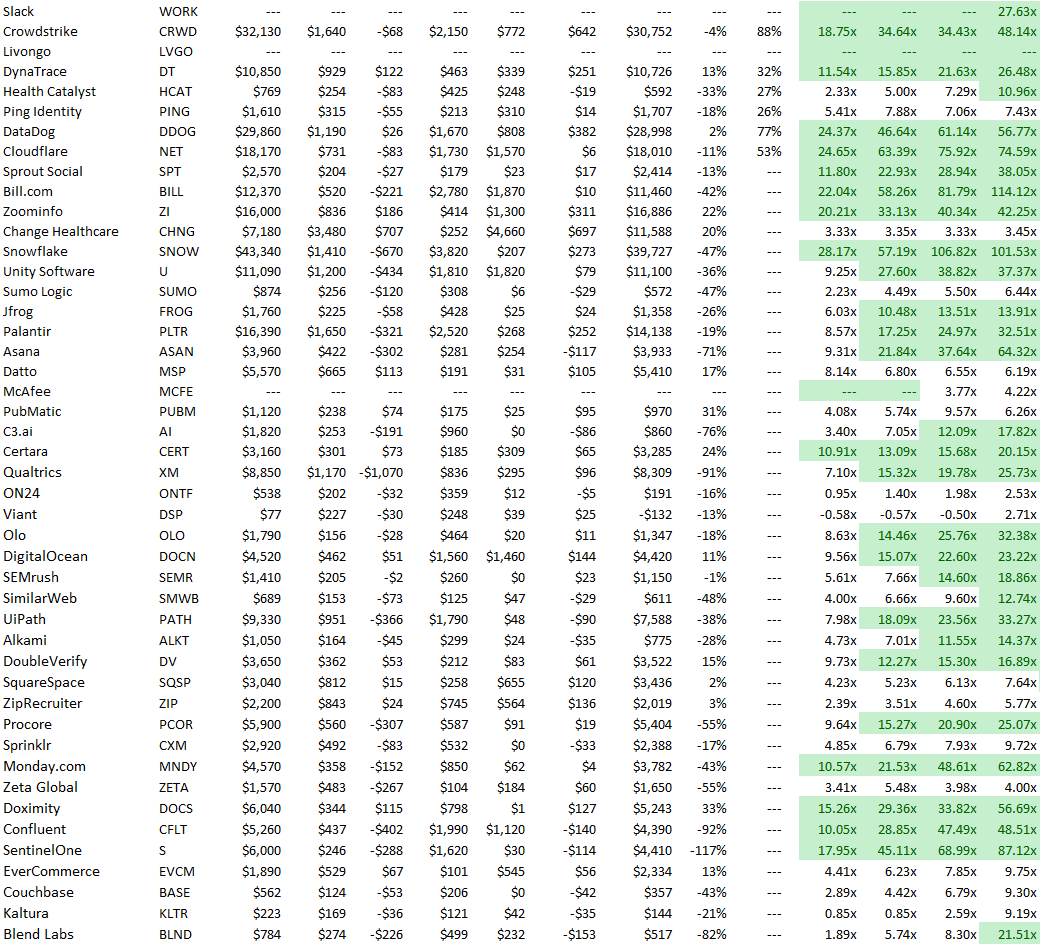

SaaS valuations have formally collapsed. We’re again to pre-2016 ranges. Of the 123 SaaS firms we observe, the typical public SaaS enterprise is buying and selling at 7.5x income whereas the median is 6.3x.

Multiples for SaaS firms rising above the median of 25% are higher: 8.4x on common and seven.9x on median.

The hole between the typical and median is 1.6x, which means premium SaaS firms are getting barely larger valuations, however that hole is lowest since Q1 2020, exhibiting the correction in overvalued names. 24% of firms are buying and selling at 10x income or higher. The knowledge is beneath.

Negative EBITDA, optimistic money circulation. The median SaaS enterprise had trailing twelve month income of $483mm, EBITDA of -$35mm, however optimistic working money circulation of $35mm due to up-front collections on annual contracts. So lengthy as you’re rising money effectively (the median annual progress price is 25%), traders will overlook detrimental EBITDA particularly if the enterprise is money circulation optimistic after working capital modifications.

The pattern. The chart beneath reveals median income multiples we’ve collected since This fall 2014. During that interval, the median SaaS a number of has ranged from 4.6x to 14.1x with a mean of 8.4x.

SaaS margins are nonetheless horrible. Investors and founders love saying “SaaS margins are great.” They’re not. They’re horrible. The median EBITDA margin for the businesses above was -12%. Fixed prices for SaaS are terribly excessive and worse but, these mounted prices are principally individuals, which means the one option to materially reduce prices is layoffs.

Premium will get a premium. Premium SaaS companies commerce at premium multiples. In the info set, 30 firms commerce at higher than 10x income, 13 commerce at higher than 15x, and solely 5 commerce at higher than 20x.

Growth is robust. The median of 25% is sweet given the scale of those firms. The common is 26%.

SaaS companies are wholesome. There is nearly no debt on these companies as banks don’t like ‘asset-lite’ companies like software program. Additionally, these firms have $463mm of money on the stability sheet on median, lots relative to annual burn (recall EBITDA is -$32mm). The variety of years of money on the stability sheet is much less essential on condition that these companies are usually money circulation optimistic (median of $35mm); solely 33 out of the 123 firms have detrimental money circulation. Note that 76 out of the 123 have detrimental EBITDA, however once more that’s acceptable as long as the expansion is current and money circulation total is optimistic.

Visit us at blossomstreetventures.com and electronic mail me immediately at sammy@blossomstreetventures.com. All founders and funds welcome! We put money into firms with run price income of $3mm to $30mm, with 12 months over 12 months progress of 20% to 50%+ relying on income. We lead or observe in progress rounds and particular conditions like inside rounds, small rounds, rushed rounds, corralling traders with our time period sheet, bridges, inbetweeners, cap desk clear up, and extensions. We can commit in 3 weeks and our examine is $1mm to $4mm. Also go to https://blossomstreetventures.com/metrics/ for all the time up-to-date SaaS metrics.