And regardless of the surge in rates of interest for auto loans.

By Wolf Richter for WOLF STREET.

The common transaction value (ATP) of latest autos bought by sellers to retail prospects in June hit a brand new breath-taking report excessive of $45,844, up by 14.5% from a 12 months in the past, and beating the prior report set in May, in keeping with estimates by J.D. Power, even as the tempo of latest automobile deliveries to retail prospects in June is anticipated to have plunged by 18% from a 12 months in the past, whereas many sellers had been brief or out of the fashions that will promote in massive numbers, as automakers proceed to battle with semiconductor shortages, triggering manufacturing shortfalls.

With general inventories close to historic lows, and barely improved from the determined ranges final 12 months, costs continued to surge, pushed by traditionally low incentives from automakers and by addendum stickers from sellers, but additionally by the prioritization of the most costly trim packages and fashions by automakers, and that’s how the ATP jumped to a brand new report.

Since June 2019, the ATP has spiked by 36%, or by over ten grand! The chart exhibits ATPs for December and June of every 12 months. Note the pre-pandemic seasonality, the place the ATP hit a excessive in December however dropped from there to June yearly. But in June 2020, the ATP was stage with December for the primary time. From then on, the ATP simply spiked with out regard to seasonality, together with this June. The inexperienced line connects the Decembers:

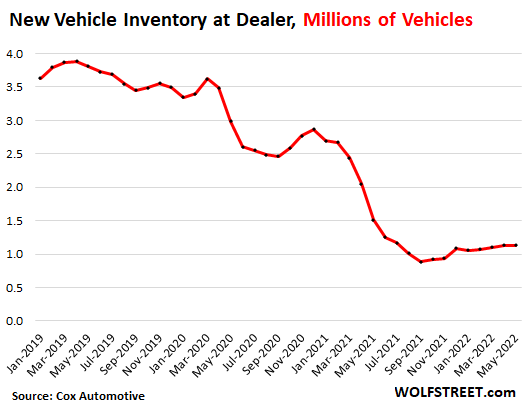

The stock nightmare.

June began out with new automobile inventories at desperately low ranges as automakers continued to battle with the semiconductor shortages that may now drag into 2023. Months in the past, many automakers stopped taking orders for sure fashions for the 2022 mannequin 12 months, the place ready lists had been so big that they can’t be constructed this 12 months, given the provision constraints. For instance, Ford stopped taking orders and reservations for the 2022 Maverick baby-truck (hybrid), the F-150 Lightning (EV), and the Mustang Mach-E (EV).

So June began out with 1.13 million new autos in stock on vendor heaps and in transit, down by 70%, or by 2.68 million autos, from the start of June 2019, in keeping with separate reporting from Cox Automotive, based mostly on its Dealertrack information. In all of 2019, the brand new automobile stock averaged 3.66 million autos, with many fashions merely out of inventory and never even orderable. Starting a number of months in the past, a further stock drawback cropped up: Customers, mauled by spiking gasoline costs, began switching to extra gas environment friendly vehicles and compact SUVs that nobody was ready for, and sellers ran out.

So, report per-vehicle gross income at sellers.

The mixture of sufficient demand that can not be constructed because of the semiconductor shortages and these traditionally low stock ranges that resulted in report excessive ATPs allowed sellers to make report per-vehicle gross income.

Total gross revenue per automobile delivered – which incorporates gross revenue from the automobile plus the revenue from finance and insurance coverage gross sales (F&I) – jumped to a report of $5,123, up by $1,174 from the already sky-high ranges of June 2021, in keeping with J.D. Power estimates. This per-vehicle gross revenue at sellers is over 2.5 occasions of what it was in the conventional occasions of June 2019.

At the per-vehicle stage, the quantities of cash made by sellers are simply astounding, as customers pay it doesn’t matter what, together with big-fat addendum stickers. This is a mirrored image of the inflationary mindset, and sellers and automakers alter pricing to benefit from it. Consumers might simply as nicely go on a consumers’ strike and refuse to purchase or order at these ridiculous costs, which might finish these value spikes, however they haven’t but.

These large per-vehicle gross income allowed all sellers mixed to make $4.9 billion in mixture in their gross sales departments, up by 10% from June final 12 months, and the fourth largest revenue for any month, regardless of the plunge in quantity.

Automakers slashed incentives to report lows, lease incentives died.

The common quantity that automakers spent on incentives, both paid to sellers or rebated to retail prospects, dropped by 59% from the already lowest ranges on report a 12 months in the past, to simply $930 per automobile on common, the second month in a row below $1,000, in keeping with J.D. Power estimates. This consists of incentives for leases, and people have been eradicated fully.

Incentive spending as a p.c of MSRP in June dropped to a report low of about 2% of MSRP. By comparability, again in 2019, incentive spending was in the vary of 10% of MSRP.

Incentive spending is how automakers alter costs for the reason that MSRPs are set at the start of the mannequin 12 months and are usually not modified in the course of the mannequin 12 months.

This large discount of incentive spending interprets into big per-vehicle gross income for automakers.

Affordability? Forget it.

The common rate of interest on new automobile loans rose to over 5% in June, in keeping with J. D. Power estimates. And regardless of report excessive trade-in worth because of the ridiculous spike in used automobile costs, which deliver down the quantity to be financed, the typical month-to-month fee jumped by 12.8% from June final 12 months.

But at this level nonetheless, customers who can afford it pay it doesn’t matter what to get a brand new automobile, and plenty of of them now order it, and so they pay addendum stickers, and so they pay larger rates of interest, and demand nonetheless exceeds provide.

Most customers might simply as nicely drive what they have already got for one other 12 months or two or 5, which makes new autos a discretionary buy, not like meals. And customers might react to those costs and rates of interest, however they haven’t but, which exhibits that the inflationary mindset is operating wild.

At some level, the Fed’s future price hikes might lastly result in auto-loan rates of interest which are so excessive that they’ll lower demand beneath the extent of provide, permitting inventories to construct, and costs to settle, and inflationary pressures to recede, however not but.

It stays exhausting to see what precise demand could be below these situations if provide had been again to pre-pandemic regular ranges. And all this exhibits is that inflationary pressures in new autos are usually not but receding as a result of sufficient customers proceed to play alongside.

Enjoy studying WOLF STREET and wish to assist it? Using advert blockers – I completely get why – however wish to assist the positioning? You can donate. I recognize it immensely. Click on the beer and iced-tea mug to learn how:

Would you wish to be notified through e-mail when WOLF STREET publishes a brand new article? Sign up right here.

![]()