In the midst of the 2022 plan yr, the medical insurance market continues to see growing and unpredictable prices, massive numbers of uninsured people, and insufficient entry to care. The American Action Forum’s Center for Health and Economy (H&E) is devoted to assessing the impression of proposed reforms that try to handle these points. The following report particulars the newest updates to the H&E baseline estimates of insurance coverage protection, federal budgetary impression, plan selection, and the premium panorama of medical insurance for Americans beneath the age of 65.

KEY FINDINGS:

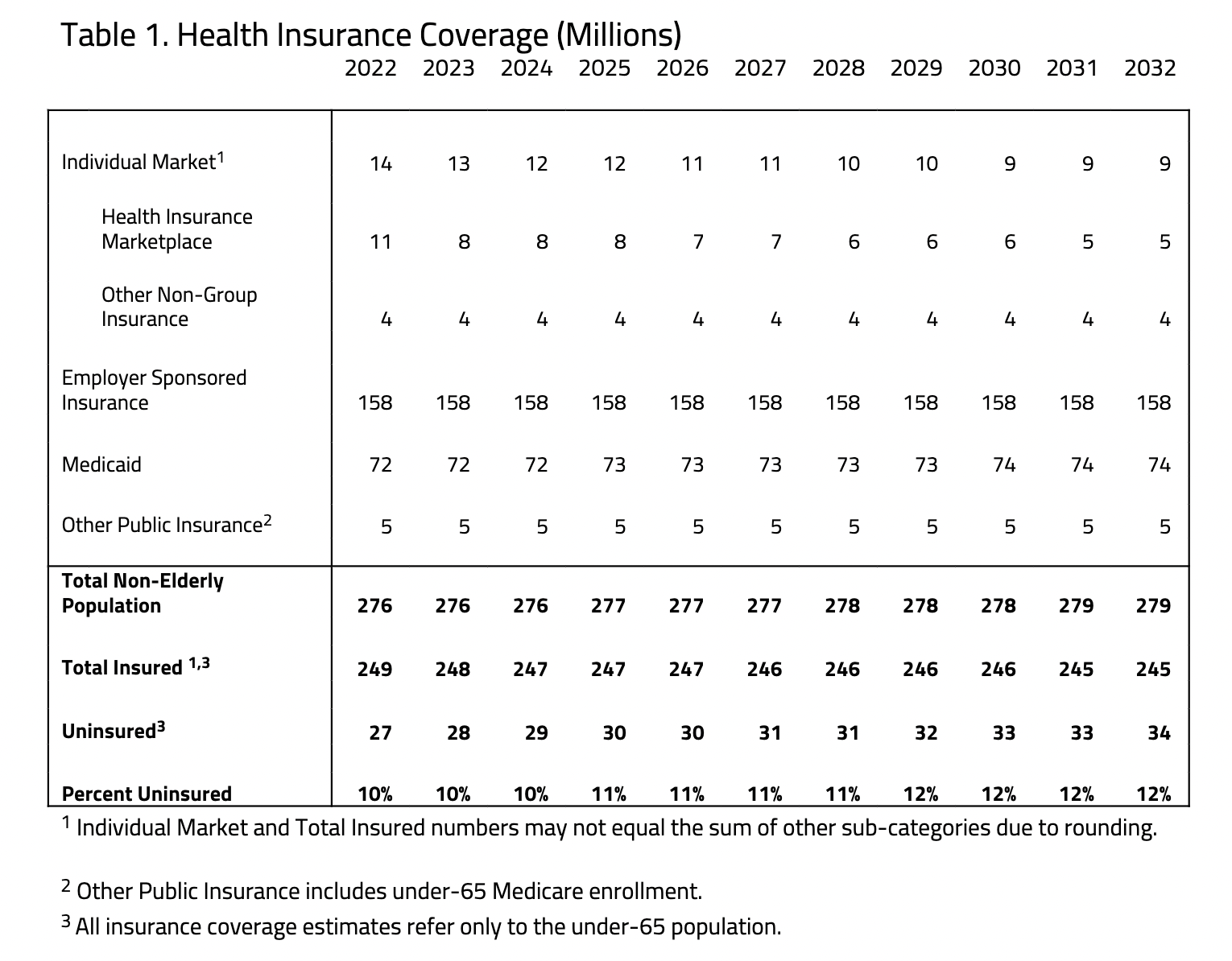

- It is estimated that the person market consists of 14 million members in 2022, with 11 million lives coated via backed insurance coverage provided within the Health Insurance Marketplace. The whole dimension of the person market is estimated to say no all through the price range window—sinking to 9 million in 2032.

- As premiums and well being care prices rise, plans chosen within the particular person market are anticipated to shift towards decrease price choices. Highly backed enrollment in Silver plans is projected to fade as a share of enrollment on the person market, whereas enrollment in Bronze plans grows amongst each backed and unsubsidized customers.

- The medical insurance protection provisions beneath present legislation for the non-elderly are estimated to extend federal outlays by $7.06 trillion from 2022 via 2032.

INSURANCE COVERAGE

H&E estimates there are 249 million non-elderly US residents with medical insurance in 2022—90 % of the overall non-elderly inhabitants. Estimates of medical insurance protection embody 4 main classes: the person market, employer sponsored insurance coverage, Medicaid, and different public insurance coverage. The particular person market is split into two subsets: backed and unsubsidized protection. Subsidized protection is bought via the Health Insurance Marketplace, and unsubsidized protection is comprised of comparable insurance coverage bought both immediately from the insurer (represented in Other Non-Group Insurance) or via the Marketplace with out monetary help. H&E makes no distinction between unsubsidized enrollees via the Marketplace and households that buy particular person market insurance coverage immediately from an insurer. Estimates regarding Medicaid additionally embrace beneficiaries of the Children’s Health Insurance Program. Other public insurance coverage is primarily comprised of Medicare protection for disabled individuals, but additionally consists of Tricare, the Indian Health Service, and different federal well being care packages for particular populations.

The enrollment for the Health Insurance Marketplace in 2022 is partially calibrated to the effectuated enrollment reported by the Centers for Medicare and Medicaid Service (CMS) for the 2021 program yr. In 2022, we estimate there are 27 million uninsured. This is roughly 1 million lower than our earlier estimates because of the impression of the COVID-19 aid invoice (The American Rescue Plan) signed into legislation in 2021with enhanced premium subsidies in 2021 and 2022. By 2023, the variety of uninsured, non-elderly Americans is projected to extend to twenty-eight million—10 % of the overall non-elderly inhabitants. The lower in insured Americans is primarily the results of 2023 premium will increase within the particular person market as the improved subsidies sundown. The common inhabitants of non-elderly Medicaid beneficiaries is estimated to be 72 million in 2022 and will rise to 74 million by 2032.[1] These estimates are topic to the uncertainty of every state’s determination relating to Medicaid growth.

H&E doesn’t make any assumptions about future state take-up of the Medicaid growth because of the many variables concerned in projecting the magnitude of the consequences of potential future expansions. Because of this, the Medicaid enrollment and spending mirrored on this baseline solely replicate the projected prices and enrollment of the Medicaid program if it have been to stay because it presently is.

The particular person market is estimated to say no from 14 million coated lives in 2022 to 9 million in 2032, pushed by premium will increase within the Marketplace. The lower in protection via the person market is partially offset by a rise in these insured via Medicaid.

As seen in Table 1, the variety of people with unsubsidized, particular person market insurance coverage is predicted to proceed on the similar stage at 4 million from 2022 to 2032 with variations no larger than 250,000 to 500,000. Rising prices and greater revenue contributions for backed enrollees are estimated to result in greater uninsured numbers later within the evaluation interval.

PREMIUMS

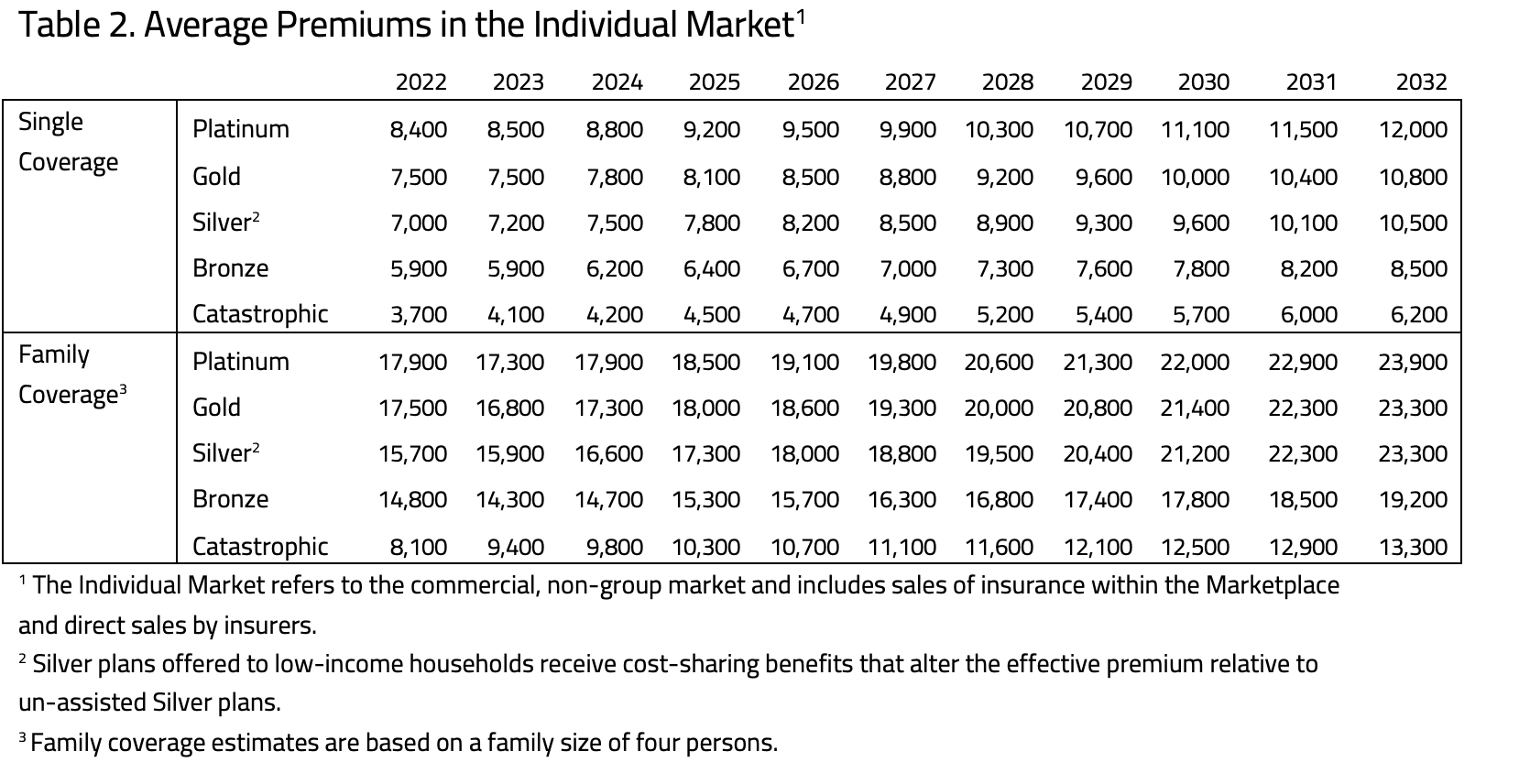

Estimates of the subsidy-eligible premiums out there within the Marketplace are calculated utilizing publicly out there knowledge on plans provided within the 33 Federally Facilitated Marketplaces. Premium estimates for unsubsidized medical insurance are calculated from a pattern of plans out there via the Robert Wood Johnson Foundation.[2] In each circumstances, H&E makes use of the default age ranking curve put forth by the Department of Health and Human Services and by particular person states to impute the relevant premium for a family. For simplification and comparability, H&E makes use of a typical household dimension of 4 (two adults and two kids) when estimating household premiums. Subsidy funds and tax income are adjusted for the suitable common household dimension in price range impression estimates.

Subsidized insurance coverage provided within the Marketplace are divided into 4 classes— Platinum, Gold, Silver, and Bronze—that correspond to 4 approximate actuarial values—90 %, 80 %, 70 %, and 60 %. The actuarial worth refers back to the anticipated share of annual medical bills coated by the insurance coverage plan.

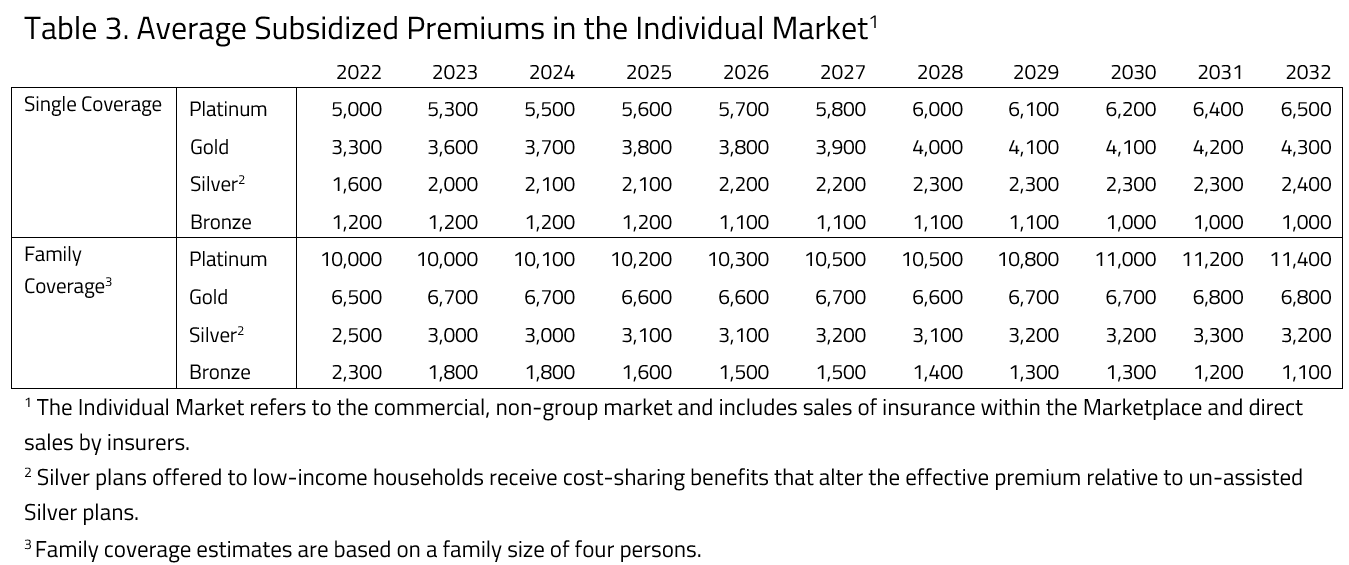

For 2023 to 2032, eligible households with incomes as much as 400 % of the Federal Poverty Level (FPL) could buy backed protection with family contribution capped at a specified share of family revenue that ranges from 2.01 to 9.56 %, relying on revenue. For 2022, there isn’t any revenue cap on eligibility and the contribution limits as a share of family revenue vary from zero to eight.5 %, relying on revenue. A federal subsidy pays the remaining portion of the premium that’s not coated by the family’s specified revenue contribution. This specified revenue contribution can be topic to annual will increase if the annual enhance in medical insurance prices exceeds a measure of family revenue development.

It is necessary to notice that, due to further cost-sharing help, the plan designs categorized as Silver fluctuate considerably in actuarial worth throughout totally different revenue classes. H&E estimates the unsubsidized premiums for these high-value Silver plans utilizing the true actuarial worth of the plan, fairly than the Silver plan value.

Unsubsidized insurance coverage, bought within the Marketplace or immediately from an insurer, are comparable in design and value to these eligible for subsidies. The ACA requires that each one medical insurance plans meet sure necessities to certify as certified protection.

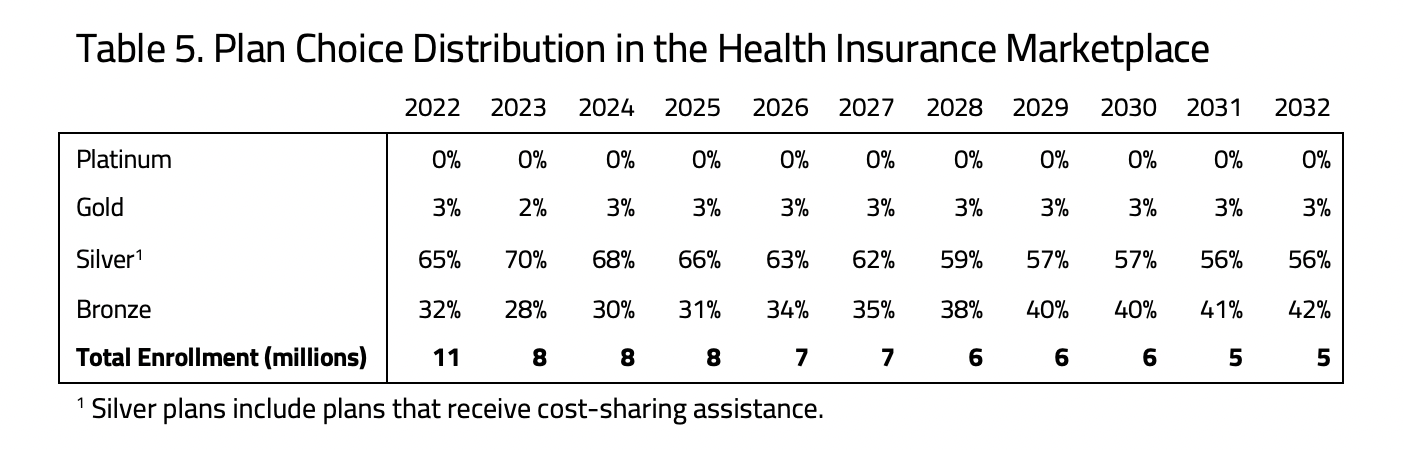

PLAN CHOICE

H&E assumes an underlying medical insurance price development of 5 % all through the remainder of the ten-year window as premium will increase have been above 5 % between 2014 and 2019 and are projected to extend at comparable ranges shifting ahead.[3] Actual year-over-year premium development estimates fluctuate because of modifications within the enrollment combine and different elements. Due to rising relevant revenue contribution charges, backed premium development for some plan designs is predicted to exceed the underlying medical insurance development price.

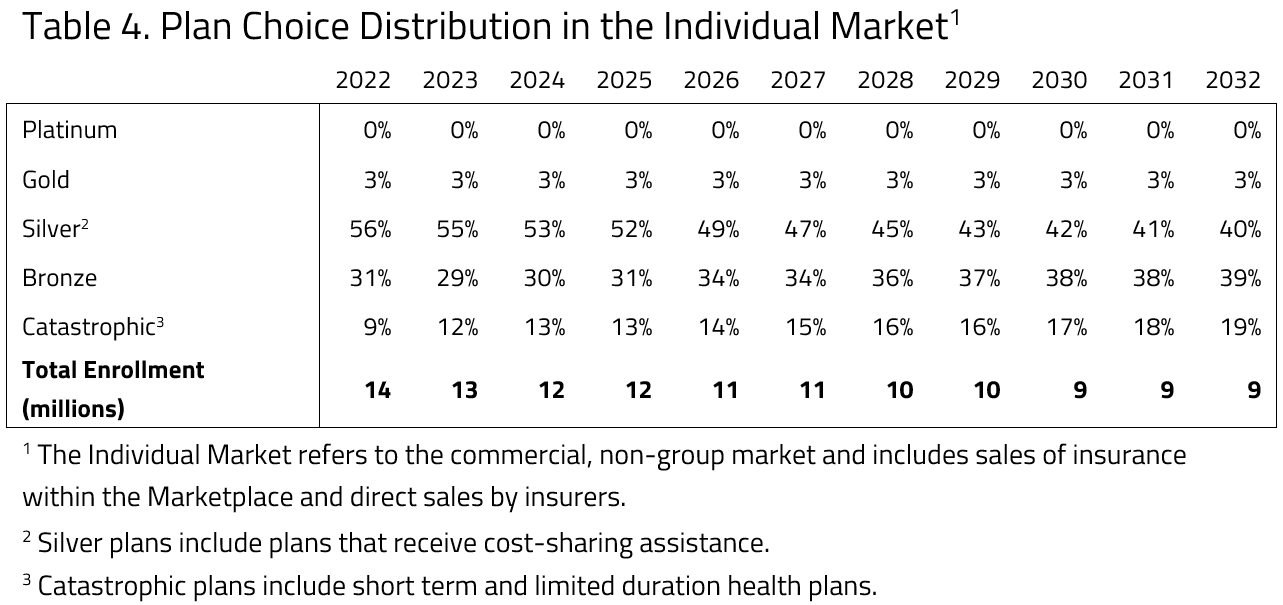

H&E makes use of the backed and unsubsidized Marketplace enrollment in every metallic stage after the primary yr to calibrate plan preferences within the particular person market and estimate plan selections all through the ten-year evaluation window.

H&E estimates that the massive enrollment in Silver plans in 2022 amongst backed insurance coverage will give technique to greater enrollment in Bronze plans as premiums rise and customers with much less beneficiant subsidy quantities modify to greater premiums. The massive majority of Silver plan enrollment is estimated to be largely comprised of households eligible for further cost-sharing advantages. As the market grows to incorporate extra households which can be eligible for premium credit the distribution of backed enrollment among the many 4 metallic ranges is predicted to turn into much less evenly distributed later within the price range window.

Beyond 2022, decrease price insurance coverage are estimated to realize market share, shifting away from extra beneficiant plans in response to the steadily rising price of medical insurance. Throughout the price range window, Silver plan enrollment is predicted to dominate {the marketplace} as price sharing advantages are solely out there for Silver plans within the Health Insurance Marketplace. As time passes and premiums rise, nevertheless, enrollment in Bronze plans are anticipated to extend.

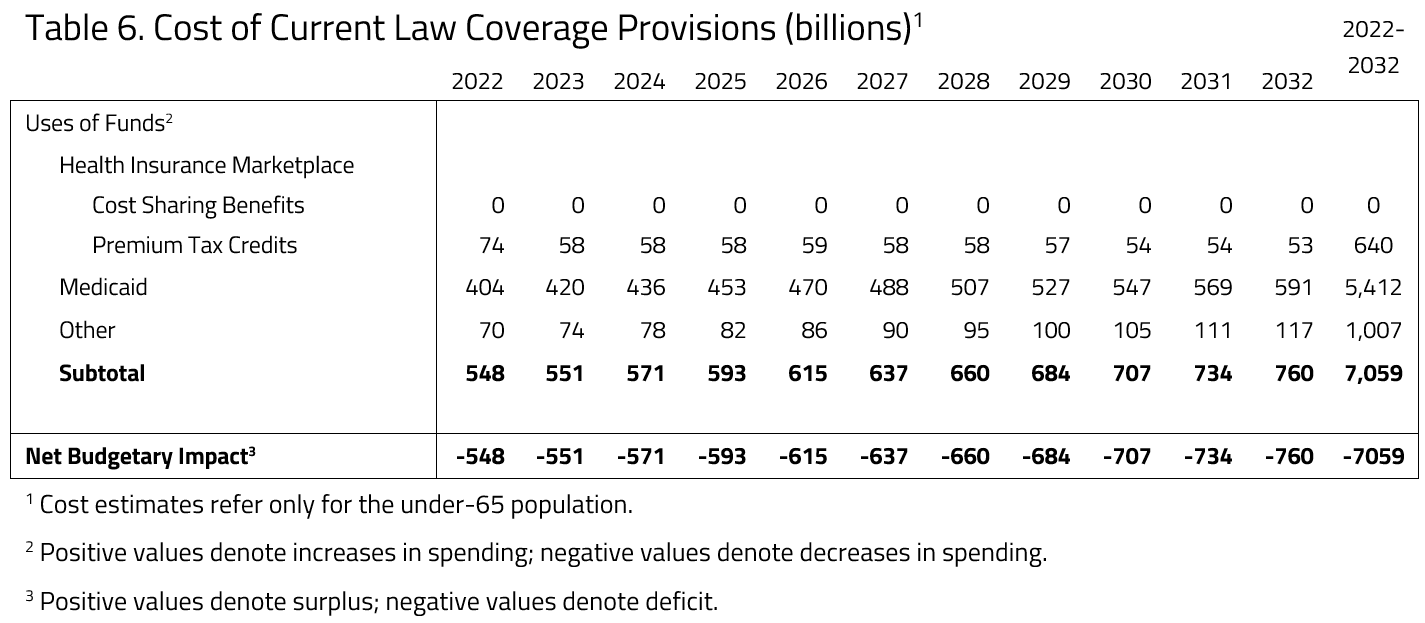

BUDGET

H&E estimates the impression on the federal price range of the key medical insurance protection provisions of present legislation with reference to the non-elderly inhabitants. Budget impression estimates don’t embrace estimates for non-ACA tax expenditures encoded in present legislation, such because the employer sponsored medical insurance tax expenditure.[4],[5]

Medicaid protection and expenditure estimates are calculated primarily based on the variety of states that had chosen to implement Medicaid growth by January 1, 2022. These predictions are delicate to future state-level selections on growth in addition to new program waivers that alter the design of a state’s Medicaid program. Over the last decade spanning between 2022 and 2032, H&E estimates that non-elderly protection provisions beneath present legislation will price $7.06 trillion.

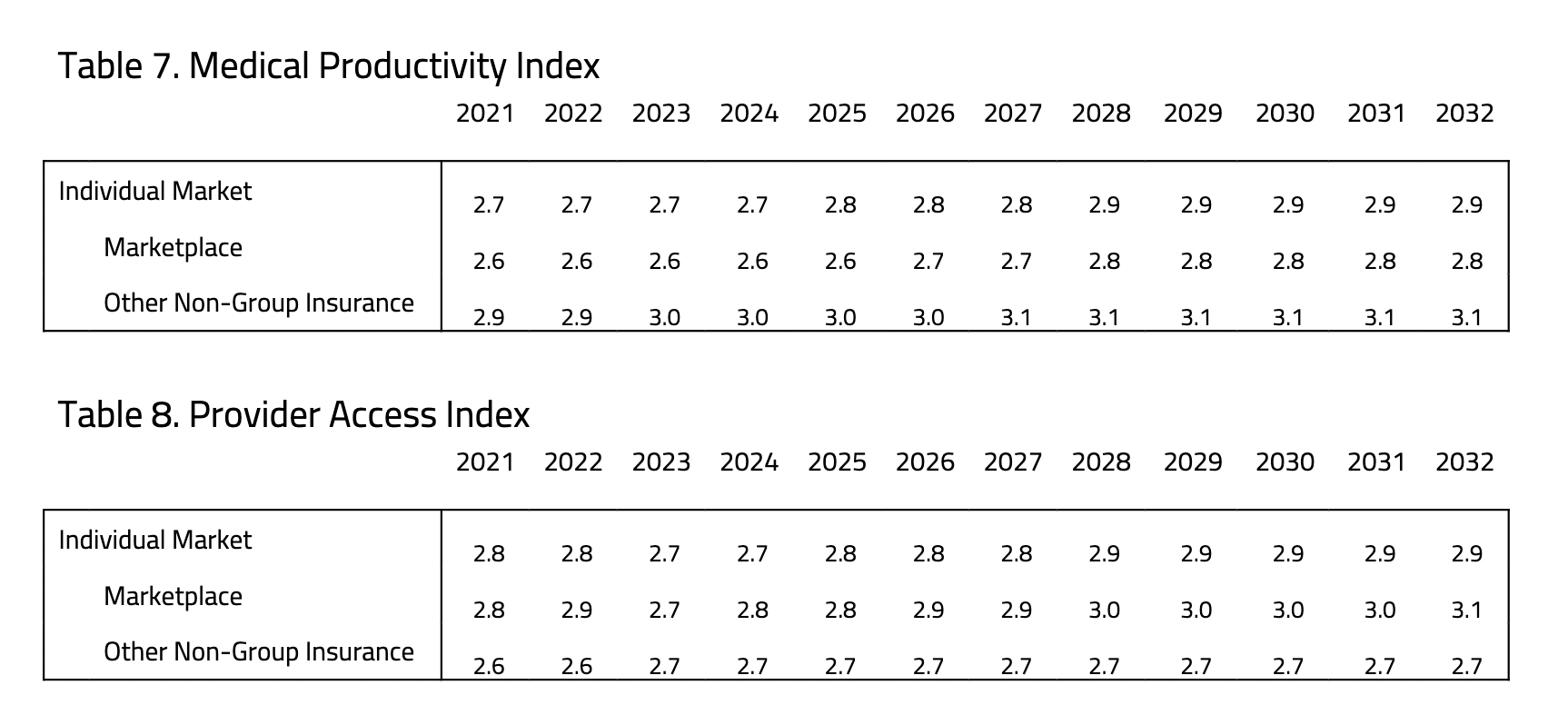

PRODUCTIVITY AND ACCESS

The Medical Productivity Index (MPI) is designed to replicate the anticipated beneficial properties in well being standing in return for medical expenditures. Plan designs that encourage sufferers to contemplate the worth of therapy when making well being care selections, reminiscent of high-deductible plans, are ascribed excessive MPI scores and vice versa. The index ranges from a low of 1.0 to a excessive of 4.0.

The Provider Access Index (PAI) is designed to replicate the supply of main and specialty physicians and services. Plans with massive networks, reminiscent of Platinum plans provided within the particular person market, are ascribed excessive scores for offering distinctive entry. Bronze and different low-cost plans that afford entry solely to restricted networks are ascribed low PAI scores. The index ranges from a low of 1.0 to a excessive of 5.0.4

CHANGES FROM PREVIOUS BASELINE ESTIMATES

As a company, H&E is continually reevaluating the assumptions and technical strategies which can be used to create baseline and proposed estimates of medical insurance protection provisions beneath present legislation. This publication is the eleventh complete baseline report, and the ninth to incorporate detailed estimates on the web budgetary impression of the ACA and Medicaid for people beneath 65.

For this baseline, H&E up to date the under-65 microsimulation mannequin. Just just like the mannequin utilized in earlier estimates, the brand new under-65 mannequin employs micro-data out there via the Medical Expenditure Panel Survey to investigate the consequences of well being insurance policies on the medical insurance plan selections of the under-65 inhabitants and interpret the ensuing impression on nationwide protection, common insurance coverage premiums, the federal price range, and the accessibility and effectivity of well being care. The up to date mannequin makes use of latest built-in non-public medical insurance selection knowledge that enables H&E to make improved predictions relating to the person market.

UNCERTAINTY IN PROJECTIONS

The Center for Health and Economy makes use of a peer-reviewed micro-simulation mannequin of the medical insurance market to investigate varied elements of the well being care system. And as with all financial forecasting, H&E estimates are related to substantial uncertainty. While the estimates present good indication on the nation’s well being care outlook, there are a variety of attainable situations that may consequence from coverage modifications, and present assumptions are unlikely to stay correct over the course of the following ten years.

Aside from the potential coverage modifications, premium will increase within the particular person market are a considerable space of uncertainty on this report. In May 2021 it was reported by the Centers for Medicare and Medicaid Services that new enrollment in the course of the Special Enrollment Period mixed with further subsidies for the Marketplace in 2021 and 2022 plans years yielded almost a million new enrollees.[6] Our estimates replicate this impression as effectively, however it is very important observe that our estimates are internet enrollment for an annual interval versus a quarterly report of latest plan enrollment. Premiums might additionally lower if Congress have been to acceptable funds required by legislation to help insurers past plan yr 2022 with the burden of providing plans with elevated price sharing help.

[1] H&E’s technique for estimating Medicaid enrollment was additionally a part of the under-65 mannequin replace. As a consequence, Medicaid enrollment is greater than in earlier baselines, accounting for the entire under-65 Medicaid inhabitants aside from these which can be dually eligible for Medicare and Medicaid.

[2] Accessed at: https://www.hixcompare.org/

[3] Centers for Medicare and Medicaid Services. National Health Expenditure Data. Accessed at: https://www.cms.gov/Research-Statistics-Data-and-Systems/Statistics-Trends-and-Reports/NationalHealthExpendData/

[4] The CBO estimates that the tax exclusion for employer sponsored insurance coverage will price $3.4 trillion over 10 years. See Distribution of Major Tax Expenditures within the Individual Income Tax System, Congressional Budget Office, May 2013, at: http://www.cbo.gov/sites/default/files/cbofiles/attachments/43768_DistributionTaxExpenditures.pdf

[5] In previous baselines, H&E has included varied estimates associated to the employer sponsored insurance coverage market that included: the excise tax on high-cost employer sponsored plans, Medical Productivity within the employer market, and Provider Access within the employer market. These have been overlooked of this baseline because of the replace of the under-65 mannequin.

[6] https://www.nytimes.com/2021/05/06/upshot/obamacare-signups.html