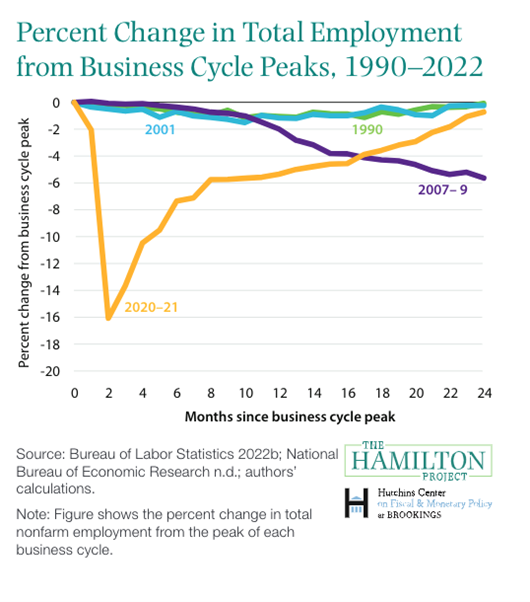

The COVID-19 pandemic resulted in the sharpest and most synchronized discount in world economic exercise in historical past. The U.S. economic system skilled a V-shaped restoration of a kind not seen in latest recessions. The speedy restoration was resulting from two elements. First, the recession itself was brought on by a shock related to COVID-19; as that shock retreated—and folks learned to higher stay with the pandemic—the economic system was poised to get better rapidly, simply because it usually does after pure disasters. Second, the coverage response protected family incomes and stored many companies intact in order that they had been able to renew extra regular ranges of economic exercise when it was protected to take action.

Real disposable private incomes truly rose in 2020 and 2021 as switch funds from the authorities vastly exceeded misplaced incomes from different sources. As a consequence, poverty, after accounting for taxes and transfers, fell in 2020 to the lowest degree since the knowledge collection started in 1967. Initially, observers and policymakers fearful {that a} cascade of bankruptcies and defaults might precipitate a monetary disaster. But enhancements to make the monetary system extra resilient in the wake of the world monetary disaster and the coverage response to the COVID-19 disaster rapidly addressed potential points.

The economic system skilled main unintended effects from the pandemic and related coverage response, most notably the highest inflation price in 40 years, far outpacing the improve in wages and resulting in the largest actual wage declines in many years. Ultimately, the economic coverage response to the COVID-19 recession must be judged not simply by its penalties in the spring of 2020, not what occurred over the subsequent two years, but in addition by the longer-term results, and whether or not the response will show to have contributed to a stronger and extra sustainable economic system going ahead.

Evidence on the COVID-19 economic coverage response

- The preliminary fiscal response in the U.S. was giant. It waned in mid-2020 after which surged once more in late 2020 and early 2021.

- Economic Impact Payments, Unemployment Insurance, forbearance applications on mortgages and scholar loans, and an enhanced CTC performed the largest roles in lifting family funds, whereas companies acquired assist largely via grants and backed loans.

- Even after the preliminary substantial fiscal help, observers typically anticipated a a lot slower economic restoration from the second quarter 2020 trough than truly got here to cross.

- The U.S. authorities incurred substantial debt. Moreover, inflationary pressures and the efforts to reasonable these pressures would possibly carry an finish to the growth.

- The U.S. fiscal response seems to have been bigger than every other nation.

Lessons learned from the breadth of economic policies during the pandemic

Policymakers ought to take the lesson from the previous two years that vigorous fiscal and financial coverage can enhance earnings for many households and disproportionately for lower-income households and may pace economic recoveries. However, doing an excessive amount of can have severe downsides that is likely to be troublesome to mitigate.

Macroeconomic assist for an economic system deep in recession with many underused assets can improve output and employment with little impact on inflation. But as the economic system will get nearer to its capability, extra macroeconomic assist will feed more and more into inflation as a substitute of enhancements in output and employment. Going ahead, the magnitude and timing of the response must be improved via extra computerized stabilizers, and the focusing on of the response must be as properly. The excellent news is such responses will be applied effectively if policies are developed upfront of a disaster.

Policymakers ought to take the lesson from the previous two years that vigorous fiscal and financial coverage can enhance earnings for many households and disproportionately for lower-income house-holds and may pace economic recoveries.

It is essential to attract classes not simply from what occurred, but in addition from what didn’t occur during the COVID-19 recession: for instance, there was no monetary disaster in the United States or worldwide. The preliminary, sturdy response by financial policy-makers was crucial to maintaining the monetary sector on an excellent keel. Better preparation in the kind of extra sturdy and stress-tested stability sheets for banks previous to the recession additionally helped.

The preexisting social security web is insufficient in the face of recessions: it isn’t beneficiant sufficient and has too many gaps, which is why it wanted to be supplemented by coverage motion each in the Great Recession and to a a lot better diploma in the COVID-19 recession. Additional computerized stabilizers are seemingly half of the reply however are unlikely to be adequate to keep away from the want for well-timed and smart discretionary fiscal responses in the future.

It remains to be not clear what policies would work higher in the United States to reduce the affect of a GDP decline on employment and protect employee attachment to their employers. Job retention schemes had been closely utilized in European international locations in comparison with state-based work sharing applications in the U.S.—these applications must be explored in better element for future downturns.