The UK has been basic to the development of open banking.

Although many countries adopted insurance policies, it was in the UK that they have been taken on at full power, sparking a revolution of challenger banks and different funds choices.

Since its conception, the UK open banking sector has gone from energy to energy. The COVID-19 pandemic accelerated an already fast-paced development, and innovation has given rise to a lot growth.

The sector as we all know it at the moment was born from the introduction of the Payment and Services Directive 1 (PSD1). In 2009 this regulatory initiative was launched by the European Union to stimulate competitors in the monetary companies {industry}.

Its later growth into Payments Services Directive 2 (PSD2) was the catalyst in the evolution of the funds and banking sector into trendy Open Banking.

Although the laws was directed at the complete of the European Union, the UK took it one step additional. Regulatory help, simplification, and cooperation between the authorities, tech, and monetary markets created a fertile setting for innovation.

Over 5 million UK residents and small companies are lively customers of open banking-enabled merchandise with 336 regulated suppliers (as of February 2022).

Coordination between the Competition and Markets Authority (CMA) and the industry-led Open Banking Implementation Entity (OBIE) has been basic to the evolution and standardization of Open Banking inside the UK.

Under the mandate of the CMA, the OBIE has carried out numerous actions involving the supervision and monitoring of information, technology of requirements, promotion of the ecosystem, and offering companies and infrastructure which are important to the working of open banking.

UK growth into open finance

After the success in the Open Banking sector, there has lengthy been a name for a transfer into Open Finance.

In November 2019, Sheldon Mills, then Director of Competition at the FCA, introduced a speech on the advantages of Open Finance.

Within the tackle, he defined Open Finance to be a part of a broader sharing initiative, with the potential to enhance entry inside monetary companies and alter the nature of competitors. A proposed focus was placed on consent administration, digital ID verification, and cross-sectoral consistency to allow consistency.

Open Finance is seen to “empower” customers, giving them extra management over their information and offering a market wealthy with competitors and innovation to meet their wants higher. It builds on the Open Banking mannequin, permitting third-party suppliers (TPPs) entry to extra monetary information throughout financial savings, mortgages, insurance coverage, client credit score, and pensions.

Work on a pensions dashboard began in 2019, not lengthy after trendy Open Banking initiatives have been launched. Still, a definitive answer is but to be launched, though current plans have been printed stating that schemes will begin staged onboarding in early 2023.

The dashboard’s gradual growth tells of the difficulties that face a sector-by-sector method to Open Finance.

“The question is, do you continue to look at it sector by sector, for example, an initiative around insurance. Or do you have a big bang approach where you say, `let’s open up data full stop.’” commented Innovate Finance Head of Policy, Adam Jackson.

There are arguments that the sector-by-sector method is just too gradual for some points, akin to local weather change options and monetary exclusion.

“GDPR has a broad look at data, but there aren’t really the legal arrangements that enable easy sharing of data across the economy. What we don’t have is the requirement for companies to publish metadata,” continued Jackson.

“We have a cost of living crisis and issues of financial exclusion where people are struggling to get access to affordable credit. The more we can do to open our data to enable people to build up credit files, the better.”

“There are arguments that these kinds of things can’t wait another seven years, so we need to look at ways of accelerating it.”

Data transparency important

The environment friendly growth of Open Finance lies basically in information transparency. For many, to allow faster implementation, continued coordination with exterior initiatives and suppose tanks is important.

In his introduction to the OBIE annual report of 2021, Imran Gulamhuseinwala OBE, the Open Banking Implementation Trustee acknowledged in the mild of the authorities announcement of its imaginative and prescient for Open Data initiatives, “The OBIE has built unique expertise and assets in these areas: it would be both sensible and beneficial for these to be utilized in these adjacent initiatives, ensuring that people and small businesses can access their data in the same safe and secure manner, regardless of product or sector.”

Alex Lempka, CEO and founding father of Connect Earth, an organization targeted on accumulating information and information transparency, stated, “The whole reason we exist is to eliminate friction in obtaining data. It’s not just fintech…we collect data to make it easy to build APIs and products. At the moment, it’s really hard to get this data (and make these products).”

On Nov. 24, 2021, The Department for Digital, Culture, Media, and Sport (DCMS) printed a coverage paper titled National Data Strategy Mission 1 Policy Framework: Unlocking the worth of information throughout the financial system.

The paper was an extension of the National Data Strategy, printed December 2020, and proposed a framework to information intervention unlocking information throughout the financial system and determine precedence areas for motion.

It marked the first step to information entry, a vital growth aspect in Open Finance.

The report recognized numerous obstacles to entry at completely different ranges, the most prevalent being issues about authorized dangers and information safety, with 39% of companies stating that this was the most vital issue stopping the sharing of their information.

Other cited elements have been lack of expertise, excessive prices, and lack of incentives.

The DCMS, with the commissioned assist of Frontier Economics, is at the moment exploring completely different ranges of information availability alongside the open information spectrum, together with ranges of entry.

Future actions targeted on supporting sector-specific trials, drawing insights from their implementation, and analysis, monitoring, and engagement with home stakeholders.

Issues with information consent

Although open finance is introduced as enabling extra competitors, issues have arisen relating to buyer discrimination on granting entry to their information and the issues talked about above on information safety.

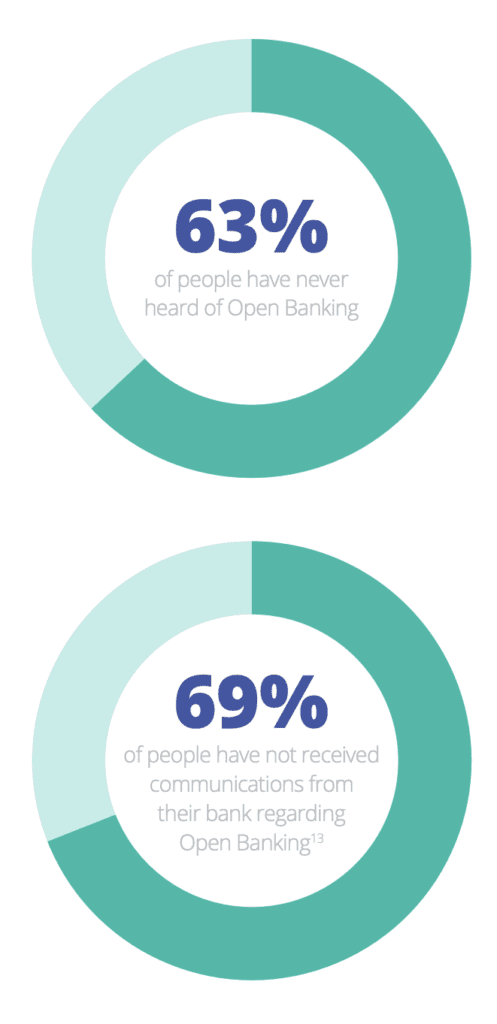

In May 2021, Zopa carried out a examine to analyze the reasoning behind client decisions not to use Open Banking. The examine confirmed that of the 37% that had heard of Open Banking, 30% acknowledged they have been involved about information privateness and vulnerability to fraud. 26% have been unwilling to open monetary data out to corporations.

The Finance Innovation Lab (FIL), a charity centered on growing the world finance sector, acknowledged that “People will only benefit from the power of their financial data if they are supported to turn it into insights that they can act on in their best interests.”

“This is a fundamental challenge given that the finance sector (including banks, fintechs, and other firms) is primarily motivated to pursue commercial gains.”

On consenting to the use of information, in many instances, customers are unaware of which particular information a number of entities will probably be in a position to entry.

With the use of computing and AI, with out correct regulation, corporations may have entry to sufficient information to “Fine-tune prices to the highest customers will accept, cherry-pick the best customers (often the wealthiest), and target adverts for inappropriate products (such as high-cost credit) to people at their most vulnerable,” as warned by the FIL.

Issues with digital literacy additionally pose issues to residents, given {that a} lack of know-how of the web and computer systems restricts entry to instruments akin to the Pensions Dashboard.

The Centre for Data Ethics and Innovation (CDEI), a subsector of the DCMS, has targeted efforts to analysis points relating to information use and belief.

Their work contains investigating the position of AI and Privacy Enhancing Technologies and the alternative for the use of information intermediaries in enabling information sharing.

The investigation has made steps in direction of establishing tips for the moral dealing with of information. Edwina Dunn, Interim chair of the CDEI, stated, “The CDEI is working in partnership with a range of organizations to help them overcome barriers, mitigate risk and put high-level ethical principles – such as accountability and transparency — into practice.”

“It’s practical work like this will enable us to build greater public trust in how data and AI are used.”

- About the Author

- Latest Posts

Isabelle is a inventive mission supervisor and freelance journalist with a BA Honours Degree in Architecture and a MA in Photography and Visual Media.

With over 5 years in the artwork and design sector, Isabelle has labored on numerous tasks, writing for actual property growth magazines and design web sites, and mission managing artwork {industry} initiatives. She has directed unbiased documentaries on artists and the esports sector and assisted in producing BBC Two’s Venice Biennale: Britain’s New Voices.

Isabelle’s curiosity in fintech comes from a craving to perceive the speedy digitalization of society and the potential it holds for our future, a subject she has addressed many instances throughout her tutorial pursuits and journalistic profession.