afsezen/iStock by way of Getty Images

Co-produced by Austin Rogers

Why Net Lease REITs? Why Today?

Often, the most effective asset lessons for buyers to purchase look the weakest or ugliest on the time they’re purchased. That is textbook worth investing. If you solely purchase the shares that everybody agrees to have a powerful outlook, you then in all probability aren’t shopping for at a really opportune worth.

That’s what makes internet lease actual property funding trusts (“REITs”) so intriguing proper now.

Net lease properties are service-oriented freestanding, single-tenant retail shops equivalent to Taco Bell (YUM) restaurant, Dollar General (DG) grocery shops, and seven/11 comfort shops:

Net lease properties (National Retail Properties)

These properties are explicit in that the tenant is liable for actual property taxes, insurance coverage, and a point of property upkeep. Rent is internet of these bills, therefore the time period “net lease.”

Another attribute trait of internet leases is the time period. Initial leases sometimes final 10-20 years with a number of possibility intervals (often 5 years every) out there for the tenant to train after the preliminary time period. Most internet lease REITs like Realty Income (O) have a weighted common remaining lease time period of round 10 years.

What’s extra, hire is often contractually mounted by way of the preliminary time period and possibility intervals with both no hire escalations or hire bumps of 1-2% yearly. This makes internet leases a company bond proxy in lots of buyers’ minds.

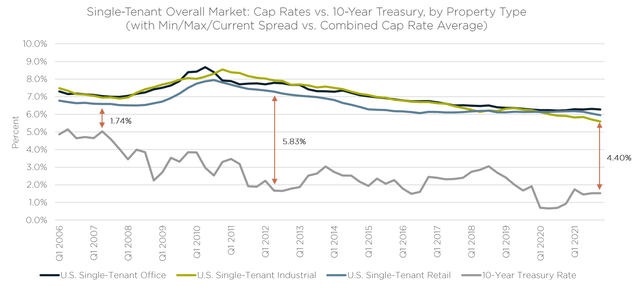

Indeed, over lengthy timespans, internet lease cap charges (internet working revenue yields) are likely to observe the motion of rates of interest, albeit with a lag of some quarters.

Net lease cap charges vs rates of interest (Stan Johnson This fall 2021 Market Snapshot)

As you may see above, internet lease cap charges transfer slower and with much less volatility than long-term rates of interest (represented above by the 10-year Treasury price). But they do ultimately go down when charges drop and go up when charges rise.

The twin arch-nemesis of internet lease REITs is an financial surroundings characterised by excessive inflation and rising rates of interest. That is strictly what we’re experiencing proper now, which the market understandably believes will harm internet lease REITs. But the market is lacking two factors:

- The unfold between cap charges and REITs’ value of debt stays on the excessive facet traditionally, giving some room for charges to rise whereas acquisitions stay accretive.

- Each time rates of interest have entered a rising cycle within the final 4 many years, they’ve topped out at decrease ranges than they have been earlier than. After topping, they ultimately drop to decrease ranges than they have been earlier than.

Given these two factors, shopping for internet lease REITs on curiosity rate-related dips has traditionally confirmed to be a good suggestion. We assume it should finally show to be a good suggestion this time as properly.

To perceive why we have to perceive the inflation menace and why it’s in all probability short-term.

The Inflation Threat

In January 2022, client inflation reached its highest stage in 4 many years, with a headline CPI print of seven.5%.

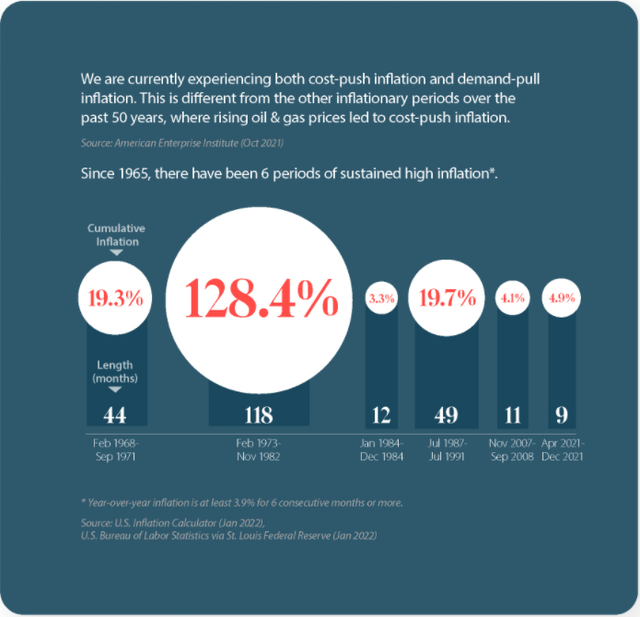

It’s helpful to recollect, nevertheless, that the cumulative rise within the CPI throughout the present bout of inflation is nowhere close to the extent of cumulative inflation skilled throughout essentially the most inflationary intervals of the final century.

High inflation intervals (Visual Capitalist)

Likewise, having lasted 10 months now, the present interval of excessive inflation remains to be the shortest interval of such inflation in current historical past – to this point, at the very least.

Note that base results (comparisons to larger costs from twelve months in the past) will start to kick in round April, which ought to put downward stress on the CPI price.

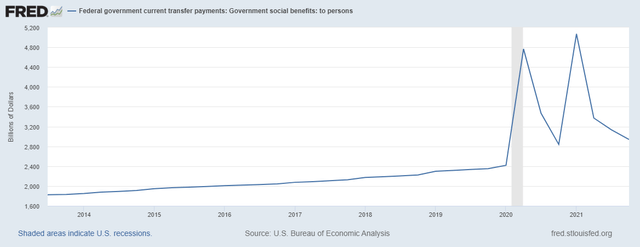

Moreover, as we defined in “Buy The Dips: High Inflation Will End Soon,” the overwhelming majority of the rise in combination demand throughout the pandemic got here from huge authorities stimulus spending, which could be seen as big spikes in authorities switch funds:

Government switch funds (Federal Reserve)

As you may see, nevertheless, with pandemic-era stimulus fading, so additionally is that this supply of combination demand.

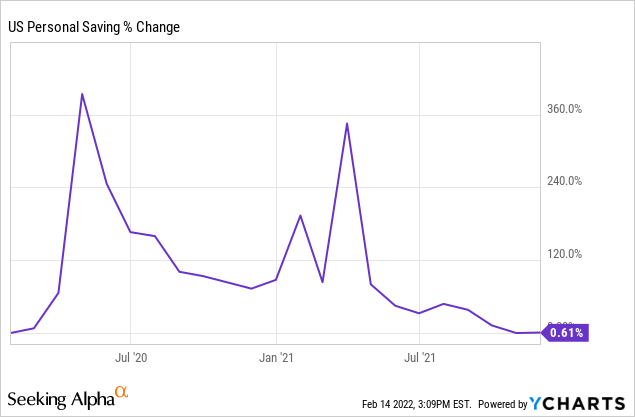

Of course, not all of this stimulus spending was spent instantly. Much of it went into financial savings accounts to be spent later. But even this stimulus-funded rise in financial savings has been completely depleted.

US Personal Saving % (YCharts)

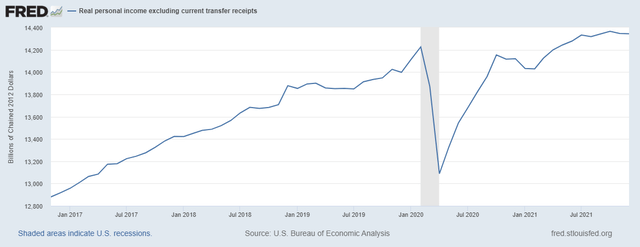

Real private revenue excluding authorities switch funds, pictured under, rose a mere 0.8% from February 2020 to December 2021, or 0.45% annualized.

Real Personal Income Excluding Transfer Payments (Federal Reserve)

Compare that to the typical annual progress in actual revenue ex. switch funds throughout the 2010s of two.9%.

In different phrases, although wages have been rising, they haven’t been rising as quick as inflation. This, mixed with diminishing pandemic-era stimulus and depleted financial savings, interprets into falling combination demand.

Of course, demand is just one facet of the inflation image. Supply is the opposite facet, and the economic system remains to be undoubtedly combating provide chain breakdowns and labor shortages.

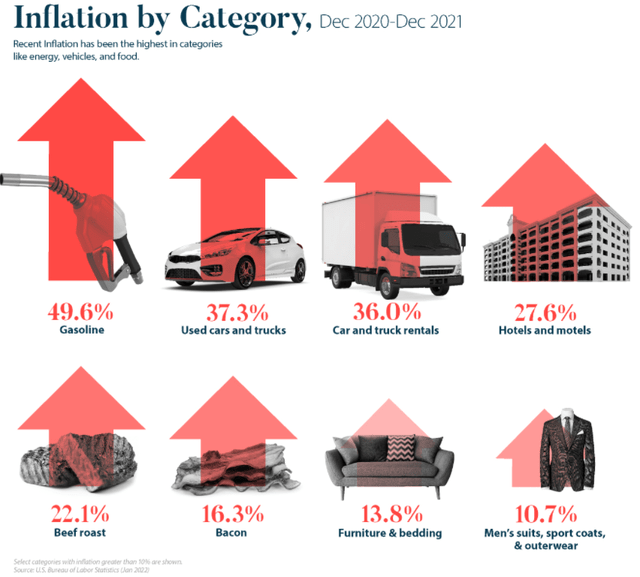

In 2021, because the economic system reopened and folks started to have interaction in out-of-home actions once more, these shortages of supplies and labor fueled big spikes in costs of assorted client merchandise.

Consumer inflation (Visual Capitalist)

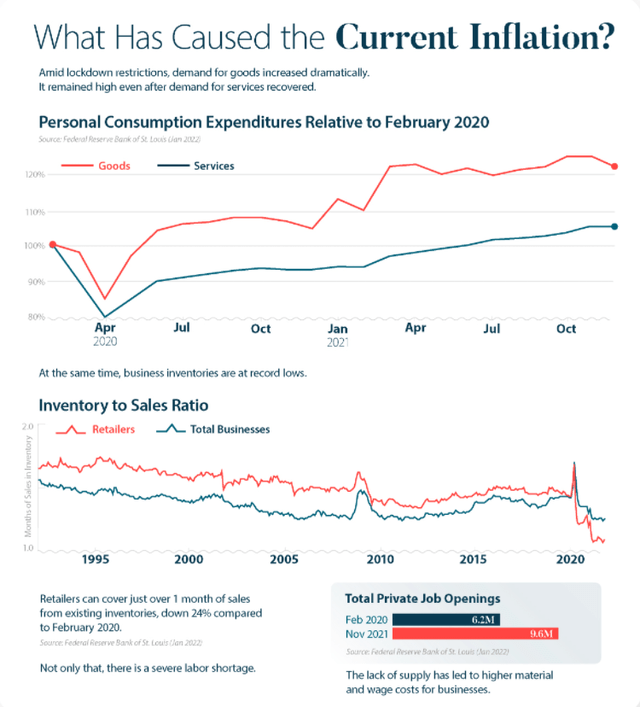

Given that in-person companies like airline flights and resort stays have been typically averted in 2021, consumption principally funneled into bodily items. This, mixed with the aforementioned provide chain issues, translated into ultra-low ranges of stock at companies typically however particularly retailers.

Inflation & stock ranges (Visual Capitalist)

What’s extra, job openings are larger than at any time in current historical past, which is fueling a rise in wages.

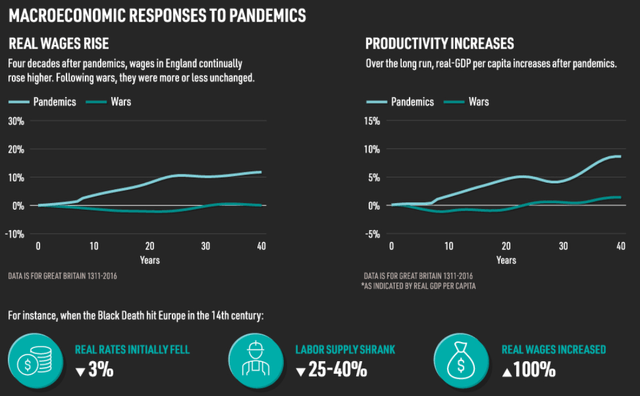

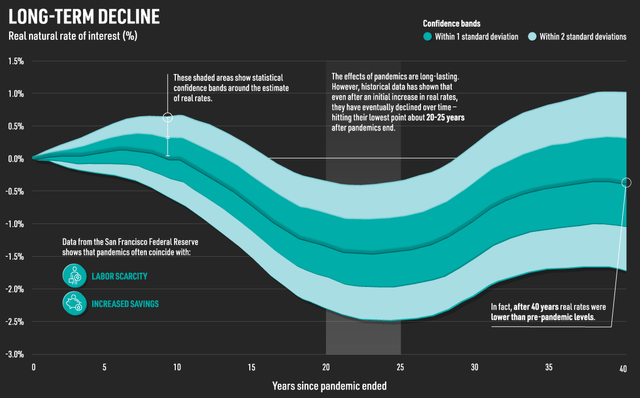

Based on a examine of pandemics going all the way in which again to the 12 months 1400, drops within the workforce due largely to deaths from the pandemic have traditionally resulted in an actual wage enhance of 10% within the 20 years following the pandemic. Likewise, productiveness (as measured by actual GDP per capita) elevated by 5% within the following twenty years.

Post-pandemic wage & productiveness progress (Visual Capitalist)

As you may see above, this contrasts with wage and productiveness will increase in post-war intervals, which traditionally are usually muted.

Despite rises in actual wages, nevertheless, you will need to observe that the examine of historic post-pandemic intervals reveals that rates of interest have a tendency to say no by about 1.5 share factors within the 20 years following the pandemic.

Interest price decline following pandemics (Visual Capitalist)

Even 40 years after the pandemic, rates of interest are usually about 0.5 factors under their pre-pandemic stage.

As demand recedes, provide chains are regularly restored, and staff return to the workforce, the distinctive COVID-19 period of the economic system ought to fade to the background and take excessive inflation charges with it.

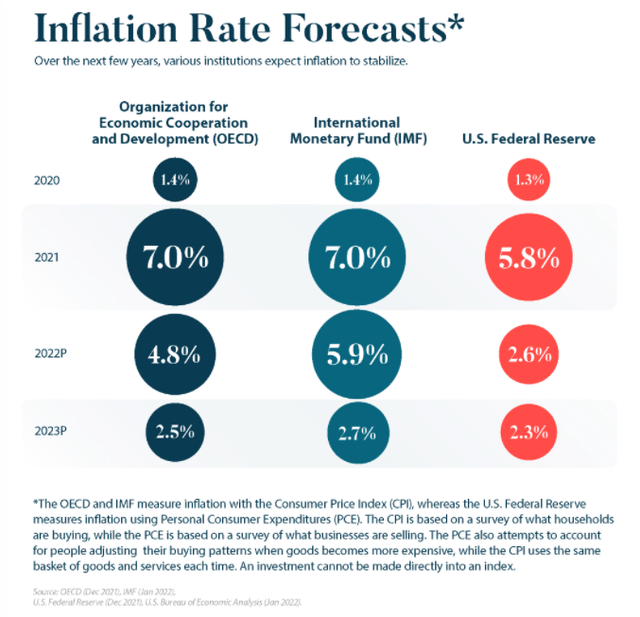

That view aligns with the forecasts of the OECD, IMF, and Federal Reserve, who see inflation ranging between 2.6% and 5.9% in 2022 after which declining again to traditionally regular charges thereafter.

Inflation forecasts (Visual Capitalist)

With getting old demographics throughout the developed world, closely indebted economies the world over, and pandemic-era stimulus now within the rearview mirror, the basic drivers of inflation now appear to be gone.

As such, it’s in all probability solely a matter of time earlier than the economic system goes again to the low inflation, low rates of interest, low progress surroundings that characterised it earlier than COVID-19.

Bottom Line

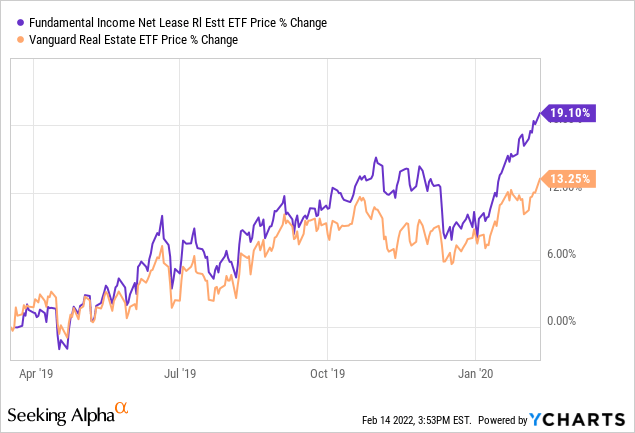

An financial surroundings characterised by low inflation, low rates of interest, and low progress is the best surroundings for internet lease REITs. This was precisely the backdrop that fueled the outperformance of internet lease REITs (NETL) over the broader REIT index (VNQ) in 2019 and the early months of 2020:

Net lease outperformance (YCharts)

Net lease REITs and comparable investments make up a substantial portion of our portfolio at High Yield Investor, and we’re assured that these holdings will proceed to gasoline outperformance in the long term.