MOZCO Mateusz Szymanski/iStock Editorial by way of Getty Images

We counsel traders to take care to not be reduce by falling knives – shares which have seen steep declines however nonetheless have additional to fall. As the market rotates away from high-flying development names to extra steady money turbines, traders want dependable basic analysis, greater than ever, to guard their portfolios from falling knives.

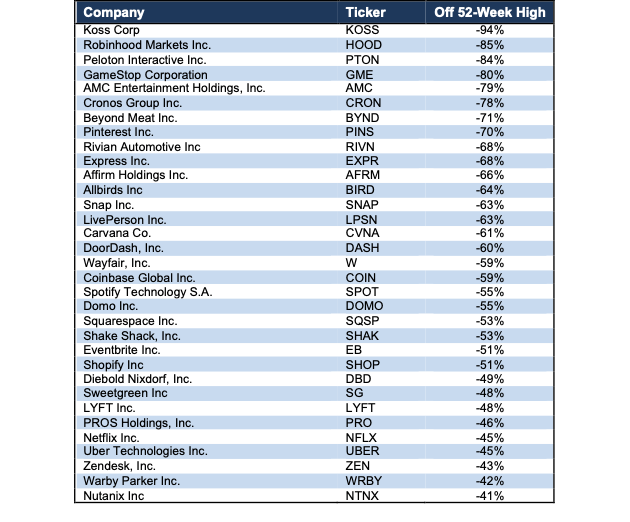

We proceed to submit an distinctive hit fee on recognizing overvalued shares. Currently, 62 out of our 65 Danger Zone inventory picks are down from their 52-week highs by greater than the S&P 500. Figure 1 lists the open Danger Zone picks which are down a minimum of 40% from their 52-week highs. Our Focus List Stocks: Short Model Portfolio, the best-of-the-best of our Danger Zone picks, outperformed the S&P 500 as a brief portfolio by 36% in 2021 with 29 out of our 31 picks outperforming the index.

This report highlights one significantly harmful falling knife: Uber (NYSE:UBER).

Figure 1: Danger Zone Picks Down >40% From 52-Week High – Performance by way of 1/28/22

Danger Zone Picks Down 40% (New Constructs, LLC)

Sources: New Constructs, LLC

Falling Knife: Uber Technologies: Down 45% from 52-Wk High & 49%+ Downside Remaining

We named Uber one of the crucial harmful shares for fiduciaries in August 2020 once we reiterated our authentic Danger Zone report from April 2019. Since our authentic report, Uber has outperformed the S&P 500 as a brief by 69% and will fall one other 49%. We element Uber’s damaged enterprise mannequin, the commoditized nature of its business, and extra challenges dealing with the corporate in our most up-to-date report.

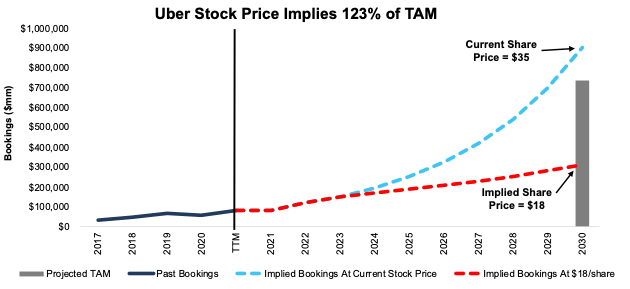

Current Price Is So Overvalued that it Implies Uber Owns 123% of 2030 TAM

Below, we use our reverse discounted money movement mannequin to investigate the expectations for future development in money flows baked into Uber’s present share value and present that it might fall 49%+ additional.

To justify its present value of $35/share, Uber should instantly:

- Improve its pre-tax margin to 4% (in comparison with -34% TTM), which is analogous to airways previous to consolidation and

- Grow income by 33% compounded yearly for the following 10 years.

In this situation, Uber would earn $189 billion in income in 2030. At its 3Q21 take fee of 21%, this situation equates to over $901 billion in gross bookings in 2030.

In different phrases, to justify its present inventory value, Uber should seize 123% of the mixed projected TAM[1] for rideshare and meals supply in 2030. For reference, Second Measure estimates Uber’s share of the U.S. rideshare TAM is 70% in December 2021 and its share of the U.S. meals supply TAM sits at 27% (together with acquired Postmates) in December 2021.

Keep in thoughts, the variety of firms that develop income by 20%-plus compounded yearly for such an extended interval are unbelievably uncommon, making the expectations in Uber’s share value outright unrealistic.

49% Downside Even if Uber Meets Industry Growth

Uber’s financial guide worth, or no development worth, is destructive $40/share, which illustrates the overly optimistic expectations in its inventory value.

Even if we assume Uber:

- Improves its pre-tax margin to six% (larger than pre-consolidation airways) and

- Grows income by 19% compounded yearly (equal to projected rideshare market CAGR by way of 2026) by way of 2030, then…

… the inventory is price simply $18/share as we speak – a 49% draw back. Even on this situation, Uber would earn $65 billion in income in 2030. At its 3Q21 take fee, this situation equates to over $310 billion in gross bookings in 2030.

This situation could even show too optimistic because it assumes a big enchancment in NOPAT margin in an business with little pricing energy because of the abundance of alternate options, by which case the draw back to the inventory can be even bigger.

Figure 2 compares Uber’s implied future gross bookings in these eventualities to its historic gross bookings, together with the anticipated TAM for rideshare and meals supply in 2030.

Figure 2: Uber’s Historical and Implied Bookings: DCF Valuation Scenarios

UBER DCF Implied Bookings (New Constructs, LLC)

Sources: New Constructs, LLC and firm filings.

Each of the above eventualities additionally assumes UBER is ready to develop income, NOPAT, and FCF with out growing working capital or mounted property. This assumption is very unlikely however permits us to create best-case eventualities that exhibit how excessive the expectations embedded within the present valuation are. For reference, UBER’s invested capital has elevated by $5.1 billion (36% of TTM income) over the trailing-twelve-months and by a median of $5.8 billion (42% of TTM income) over the previous three years.

Fundamental Research Provides Clarity in Frothy Markets

2022 has rapidly proven traders that fundamentals matter and shares don’t solely go up. With a greater grasp on fundamentals, traders have a greater sense of when to purchase and promote – and – know the way a lot danger they take once they personal a inventory at sure ranges. Without dependable basic analysis, traders haven’t any approach of gauging whether or not a inventory is pricey or low-cost.

As proven above, disciplined, dependable basic analysis reveals that even after plummeting, Uber nonetheless holds vital draw back.

This article initially revealed on January 31, 2022.

Disclosure: David Trainer, Kyle Guske II, and Matt Shuler obtain no compensation to jot down about any particular inventory, type, or theme.

[1] 2030 TAM estimate equals a $423 billion international ridesharing market and $312 billion international meals supply market. Global ridesharing TAM assumes the worldwide rideshare market continues rising at 19.2% yearly from 2026-2030 (in step with Mordor Intelligence’s estimated CAGR by way of 2026). Global meals supply TAM assumes the worldwide meals supply market continues rising at 10.9% yearly from 2028-2030 (in step with Research and Market’s estimated CAGR by way of 2028).