MOZCO Mateusz Szymanski/iStock Editorial through Getty Images

In my perspective, whereas the selloff in tech shares that has picked up over the previous few weeks has been essential to resetting valuations, it has gone manner too far in a lot of key shares.

Uber (UBER) is without doubt one of the corporations that I believe is ripe for a rebound. When I take into consideration the way forward for mobility, I proceed to view it as an inevitability that automobile possession will decline (particularly as costs rise and plenty of states push for eventual conversion to all-electric) and extra folks will flip to the comfort of rideshare for short-distance journeys. Fundamentally, the enterprise has stabilized for the reason that preliminary pandemic shocks and is well-positioned for progress.

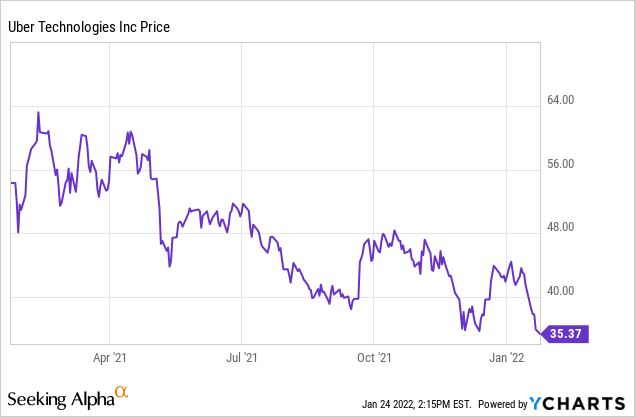

The inventory, in the meantime, has misplaced ~45% of its peak worth since notching a excessive above $60 final February. In 2022 year-to-date alone, Uber has given up one other 20%. All of that is coming alongside basic lifts and constructive updates from the enterprise finish, making a well-timed shopping for alternative.

I’m upgrading my viewpoint on Uber to robust purchase (up from my prior view of purchase) as a result of rebound alternatives made inherent by the current crash. I proceed to encourage buyers to have a long-term mindset on Uber, as the biggest rideshare firm with probably the most to learn from progress and economies of scale.

Here’s a refresher on what I view to be the important thing bullish drivers behind Uber:

- Huge $13.8 trillion TAM. Mobility and Delivery every carry $5 trillion market alternatives, and nascent Uber Freight is one other huge $3.8 trillion market that’s closely underserved and ripe for tech disruption.

- Formidable market management. In a lot of the markets that Uber operates in, the corporate has a number one market share, and often by a considerable margin. The firm has selectively exited markets the place it misplaced share to a neighborhood incumbent (Grab in Singapore is an effective instance), so it may deal with turf the place it has the benefit.

- The sharing financial system is step by step taking priority over possession. In 2021, a semiconductor scarcity has dramatically elevated the worth of automobiles, each used and new. Even earlier than this value shock and pre-pandemic, many shoppers have been already questioning the knowledge of automobile possession over rideshare. Owning a automobile comes with upkeep prices, insurance coverage prices, and in city areas, usually hefty parking prices. Gradually, I count on automobile possession to say no and for rideshare to turn into the preeminent type of transportation.

- “Other bets” are quite a few. Uber Freight is one of the best instance of a brand new initiative to drive progress, however grocery and bundle supply are others as nicely. Uber’s deal with something involving mobility offers it a large greenfield market to function in.

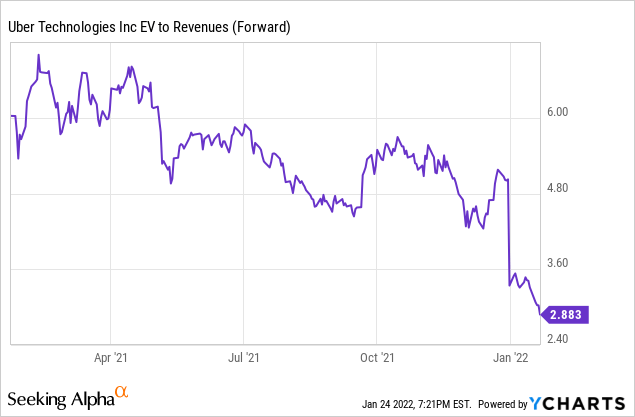

Note as nicely from a valuation entrance that Uber is presently buying and selling at a ~2.9x ahead income a number of – whereas previously it had hardly ever traded beneath a ~5x ahead income a number of.

Though Uber will take time to consolidate and rebound because the market continues to be uneven for tech names, I consider Uber has sunk low sufficient to benefit a rebound purchase. In my case, I first dipped into Uber within the low $40s and am pleased to dollar-cost common down at present ranges.

Bookings energy: rideshare has normalized, whereas supply continues to stay elevated

One of the important thing causes I stay optimistic on Uber is that the pandemic has basically modified {our relationships} to meals and meals. In the U.S., there was a noticeable shift towards takeout and supply orders, supported by the comfort of rideshare platforms like Uber Eats.

The causes for this shift are quite a few and certain range broadly from individual to individual:

- Local eating places are closed for dine-in, or prospects are nonetheless uncomfortable consuming out in the course of the pandemic

- We are not working within the workplace, substituting workplace dinners for at-home dinners

- Our lives have gotten busy, with work seemingly extra demanding than ever and oldsters juggling distant education, necessitating straightforward takeout choices

The key commentary right here is that this shift appears everlasting and right here to remain. Many eating places have adopted their enterprise fashions and staffing to accommodate the better combine towards takeout eating versus in-person eating, and ghost kitchens that assist solely takeout orders proceed to be a sizzling space for funding.

For Uber particularly, probably the most encouraging metric we’ve seen is that whereas rideshare has roughly recovered to pre-pandemic ranges, supply orders stay at vastly elevated ranges.

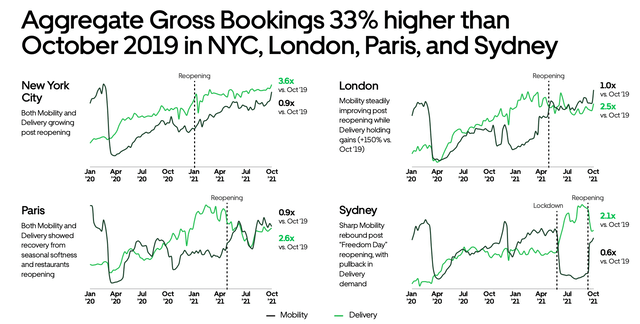

Uber bookings by market

Uber Q3 investor presentation

In markets like New York City, as proven within the chart above, rideshare bookings in October are at 0.9x pre-pandemic ranges (2019), whereas supply orders are 3.6x larger. Trends are comparable in London and Paris, the place rideshare bookings are at 0.9-1.0x pre-pandemic ranges, whereas supply is up ~2.5x over the two-year-ago interval. To me, what this implies is that Uber’s proverbial pie has grown, and Uber is taking better client pockets share as a result of desire shift towards takeout meals, whilst its rideshare enterprise is rising comparatively unscathed from the pandemic.

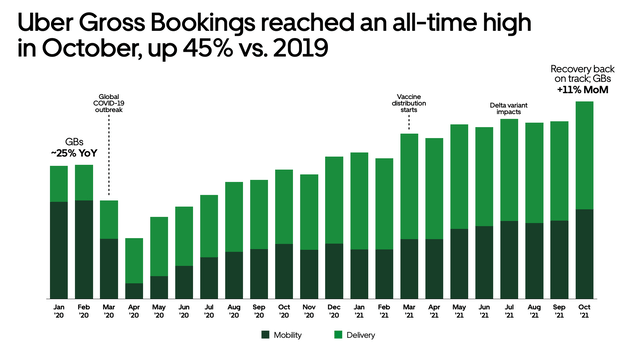

Uber whole bookings

Uber Q3 investor presentation

As a results of Uber’s capacity to maintain excessive supply ranges whereas recovering rideshare, general bookings on the platform have by no means appeared higher. In October (previous the Q3 cutoff), Uber’s gross bookings grew at a large 45% y/y tempo and reached an all-time month-to-month bookings document.

For This autumn as nicely, Uber expects gross bookings to elevate to a spread of $25-26 billion, larger sequentially versus $23.1 billion in gross bookings for Q3.

Part of the rationale why bookings have remained elevated has been Uber’s capacity to shortly chase the difficulty of driver shortages. Broadly throughout most markets, there are actually extra drivers readily available to satisfy extremely elevated supply demand. Per CEO Dara Khosrowshahi’s ready remarks on the Q3 earnings name:

When we first noticed demand starting to outstrip provide in Q2, we made a acutely aware choice to speculate quick and to speculate aggressively in attracting drivers again to Uber with a deal with the US.

The outcomes are clear, we have seen 10 consecutive weeks of energetic driver progress within the US, leading to a much better rider expertise. The variety of energetic drivers is up greater than 65% since January, and greater than 20% since June. As a consequence, the incidence of surge pricing has fallen by practically half and wait instances are actually beneath the magic 5 minute mark on common. We did this whereas meaningfully lowering incentive ranges and on the similar time, driver earnings remained close to all-time highs because of elevated utilization.

We’ve additionally continued to develop the variety of couriers on Eats within the US with energetic couriers up 80% since January and 25% since June. In different phrases, not solely are we approaching our provide and demand steadiness for Mobility within the US, we have carried out so whereas practically doubling our Delivery courier base from its low in Q1.

All-in-all, our month-to-month energetic driver and courier base within the US has grown by practically 640,000 since January. Against a backdrop of historic labor shortages and an abundance of selection for employees is a powerful endorsement of Uber’s worth and the worth of unbiased, versatile work. In a world the place flexibility has more and more turn into non-negotiable for employees throughout the financial system, we consider Uber will probably be an much more engaging choice going ahead.”

Profitability progress

Uber’s remarkable progress on profitability also bears mentioning. Prior to the pandemic hitting, one of investors’ major concerns with Uber was the fact that the rideshare/mobility segment was essentially financing and plugging the massive losses that Uber was incurring in delivery, as well as other nascent efforts like freight.

Now, with Delivery achieving economies of scale at its much greater size, Uber’s consolidated profitability has never looked better.

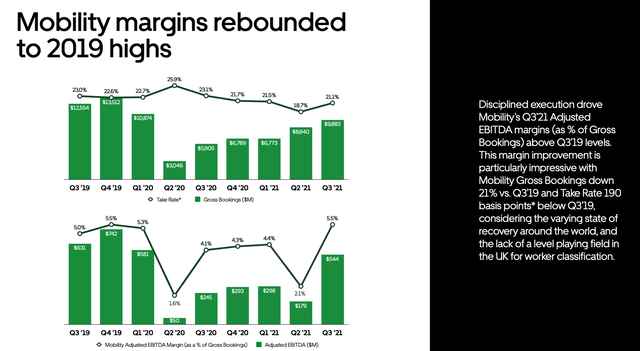

On the mobility side, given the recent rebound in rideshare bookings, the company noted that Mobility adjusted EBITDA margins have ramped back to their pre-pandemic highs above 50% (with the slight caveat that Uber measures this margin against gross bookings, instead of against revenue):

Mobility profitability

Uber Q3 investor presentation

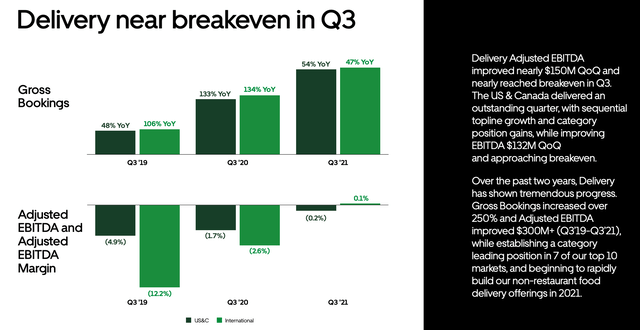

Similarly, when we strip out the delivery business, we see that both US/Canada and international delivery markets have hit a roughly breakeven adjusted EBITDA margin, versus mid-single digit/low-teens margin losses in the prior few years:

Delivery profitability

Uber Q3 investor presentation

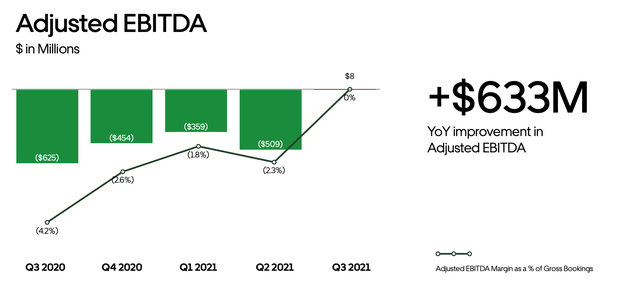

As a consolidated whole, Uber’s Q3 adjusted EBITDA reached constructive $8 million in Q3, which is a huge y/y enchancment versus a -$625 million loss (-4% margin) within the year-ago quarter:

Uber consolidated adjusted EBITDA

Uber Q3 investor presentation

And waiting for This autumn, Uber is anticipating $25-$75 million of adjusted EBITDA subsequent quarter, indicating that this can be a enterprise that is able to begin minting revenue progress as nicely.

Key takeaways

In my view, the current sharp fall in Uber’s inventory is closely misaligned with robust basic tendencies within the enterprise. In explicit, I lean on the truth that the rideshare enterprise’ bookings and profitability have reached pre-pandemic ranges, whereas supply is sustaining at a 2-3x dimension post-pandemic whereas additionally hitting breakeven. Use the dip as a shopping for alternative.