Gerville/E+ through Getty Images

Overview

I’ve seen many dialogue on Ballantyne Strong (BTN) through Twitter and different numerous blogs however have not come throughout and up to date thesis so right here we go:

The theme that can preserve being pushed house all through the write-up is a saying that’s far too overused: “head we win, tails we don’t lose much” – or to place it in “fa-nance” phrases: “downside protection with upside optionality.”

Almost each asset owned by Ballantyne Strong appears priced for a draw back or worst case situation which leaves the fairness investor with a major quantity of free embedded name choices throughout the BTN complicated.

I’m no Morgan Housel, so bear with me if the writing is a bit of dry. And I typically do not know what I’m doing, so do your individual due diligence. All greenback quantities are in USD, and costs replicate the market costs as of January 20, 2022.

Ballantyne Strong is a holding firm with 5 property:

- 100% possession in Strong Entertainment: Manufactures, sells, and gives upkeep to film theatre screens

- ~8.6% possession in InexperiencedFirst Forest Products (OTCPK:ICLTF): Seven lumber mills in Eastern Canada

- ~20% possession in FG Financial (FGF): Reinsurance and SPAC firm

- $13.0m Series A Preferred fairness funding in Firefly: Outdoor promoting firm that owns digital advert screens on prime of taxi/rideshare automobiles

- $10.5m money

2020 BTN 10-k

Key Players

The two key gamers all through BTN’s 5 property are Kyle Cerminara (“Kyle”) and Larry Swets (“Larry”). Kyle is the Board Chair and largest shareholder of BTN. He invests in BTN and firms throughout the BTN complicated via Fundamental Global Investors (FGI) which is an funding agency he has run with Joe Moglia , the previous CEO of TD Ameritrade, since 2012. FGI owns ~32% of BTN and Kyle personally owns one other ~2%.

Larry has been operating finance & insurance coverage operations and collaborating in numerous investments alongside Kyle since Larry was CEO at Kingsway Financial Services (KFS) from 2010-2018. Larry invests within the BTN complicated of corporations primarily via Itasca Financial LLC.

Below are the present roles of each Kyle and Larry:

Kyle Cerminara

- CEO of Fundamental Global Investors

- Chairman of the Board of Ballantyne Strong

- Chairman of the Board of FG Financial Group

- Board member of Firefly

- Board member of BK Technologies (BKTI)

Larry Swets

- Managing Director of Itasca Financial LLC

- Board member of Ballantyne Strong

- CEO and board member of FG Financial

- Board member of InexperiencedFirst

- Board member of Harbor Custom Development (HCDI)

Capital Allocation

There have been each constructive and adverse articles written about Kyle and Larry and their capital allocation strategies, type of investing and complexity of their investments. I’ve spent a quick period of time with each of them and some different members of the BTN workforce however as a substitute of discussing various private opinions let’s simply lay out the info.

Kyle began Fundamental Global Investors in 2012 alongside Joe Moglia. One of their main investments was BTN and by 2015 FGI had launched an activist marketing campaign as the largest shareholder.

The intention for FGI wasn’t to develop into an activist investor in BTN however it appears the failed acquisition of Convergent from Sony in 2013 for $17.4m ,after changes, by BTN’s prior administration workforce was the catalyst for FGI to go activist.

Sales of Convergent Media fell from $40m on the time of the acquisition in 2013 to $17m by 2015, extra particulars afterward.

By early 2015, Kyle and FGI had overhauled the BTN board and elements of administration and laid out a brand new total technique for BTN to “build a high performing holding company with a diverse mix of businesses that contribute to the overall cash flow of the company.”

By mid-2015, Kyle stepped in as each the CEO and chairman of the board of BTN. Kyle slowly re-positioned a few of BTN investments in order that by 2016-2017 the BTN holding firm seemed as follows:

- Strong Entertainment

- Convergent Media

- Three fairness investments made by Kyle:

PIH Property Holdings (PIH):

- $7.7m invested from 2016-2017

- Run by Larry Swets

RELM Wireless (OTC:RELM)

Itasca Capital

- $3.7m invested in 2016

- Run by Larry Swets

We will undergo the entire property above in additional element all through the write as much as assess how administration has executed since taking up in 2015 however right here is fast overview.

- Strong Entertainment: IPOing this 12 months for an undisclosed quantity

- Convergent Media: purchased for $17m from Sony in 2013 was bought for ~$17m in money in 2021. Part of Convergent was spun off which result in $9m of BTN’s $13m Preferred Series A shares in Firefly

- Three Equity Investments made by Kyle:

The $7.7m invested in PIH is now price ~$3.5m and underneath the identify FG Financial

The $4.3m invested in RELM was bought for $4.5m in 2018. RELM is now BK Technologies

The $3.7m invested in ICL is now price $13-$15m (together with dividends) and underneath the identify InexperiencedFirst Forest Products (GFP)

So, in brief, there was some good, dangerous, and nonetheless but to be decided capital allocation choices. That being stated, BTN’s market cap is down 30-40% since Kyle and FGI took over in 2015.

Kyle stated on Bill Brewster’s podcast “when an activist takes over a microcap company you should expect the next 2-3 years will be a total disaster…because they are basically going to take over the sins of the past.”

What a part of this underperformance since 2015 do you wish to attribute to administration, sins of the previous, Covid, the marketplace for Strong Entertainment declining, and so forth. is as much as you.

The necessary level I’ll attempt to proceed to drive house is given the valuation of BTN no sensible capital allocation and even mediocre capital allocation must happen. A draw back situation may occur in all 5 of BTN’s property and it appears possible buyers would get the present BTN market cap again.

Additionally, I’ll lay out the case that Kyle and Larry appear to be evolving from their previous errors of capital allocation and altering their funding method which lays the groundwork for a constructive inflection level or one of many many free embedded name choices throughout the BTN fairness valuation.

Complexity

Before we dive into the 5 property at BTN, the final two subjects price addressing are the complexity and the prices that include the BTN holding firm construction.

Kyle Cerminara and FGI have main holdings in:

- BTN: FGI owns ~32%

- FG Financial (previously PIH): FGI owns ~51%

- InexperiencedFirst Forest Products (previously ICL): FGI owns ~2%

- BK Technologies (previously RELM): FGI owns ~21%

- OPFI & HGTY: Investments through SPACs that FGI co-sponsored with FG Financial: FGI owns <1-2% possession

Kyle and Larry additionally personal smaller private positions in most of those corporations. Some of which have been acquired via inventory awards given.

Admittedly, bigger holding corporations such because the John Malone’s Liberty complicated of corporations have an advanced arrange however seeing this a lot complexity and interrelated social gathering transactions between a personal funding agency and a public microcap could make buyers squirrelly.

None of it comes off as nefarious for my part, however the intertwined funding technique of Kyle and Larry makes it very tough for buyers to prognosis if and the place they’re aligned with Kyle and Larry from a danger/reward perspective. Some of the examples embrace:

These are only a few examples of the interrelated transactions that at present exist or have existed all through the Kyle and Larry funding complicated.

I’m not highlighting this as a result of I feel one thing is being coated up, it could simply take critical in-depth evaluation ,which the typical retail investor would not have time for, to determine the place and the way BTN fairness buyers are aligned with Kyle and Larry from a danger/reward standpoint.

One of the principle dangers I see behind the complexity piece is BTN can be unable to draw the appropriate shareholder base.

From investing and following Berkshire (BRK) and Markel (MKL), I’ve seen how necessary it’s for the success of the corporate to have a shareholder base that aligns with administration. I worry that until this complexity is diminished that cautious, affected person and long-term minded buyers is not going to be part of BTN in massive numbers.

Going again to the John Malone complexity dialogue. My understanding of the complexity of Malone’s structuring all through his funding profession is as a result of his engineering thoughts is at all times targeted on lowering taxes, each bit of the complicated structuring was executed to scale back the quantity of taxes shareholders needed to pay.

As is claimed within the e book The Outsiders “To understand the company {TCI} you would have to read all of their footnotes and very few did…Malone however believed this complexity was a small price to pay for the enormous value created over the years by these projects.” “Malone was consciously increasing the complexity of his business in pursuit of the best economic outcome for shareholders.”

It’s fairly potential that a few of the incentive behind the complexities of Malone’s corporations is so he may proceed to amass possession at discounted valuations, however it has undoubtedly offered long-term shareholders worth on the identical time.

Admittedly, I’ve by no means instantly requested BTN administration the rationale behind the interrelated social gathering transactions and complexity, however I can’t unpeel how it’s a web profit.

There is nearly definitely some benefit to compiling microcap corporations collectively right into a holding firm to scale back overhead prices, however I’m unsure the issue it has created for the potential shareholders to worth and assess BTN makes this a web profit. The complexity nearly definitely has and can make it more durable for BTN administration to boost capital. This seemed to be the case when BTN administration raised capital in 2021 at suppressed market costs though this manner throughout a pandemic to be truthful.

Again, I view this as a “head we win, tails we don’t lose much” state of affairs. Even if the complexity and problem valuing BTN stays, it’s possible we get not less than the present market cap again even when the draw back situation happens in all 5 BTN property.

It seems to me that Kyle and BTN administration are working to scale back complexity which we’ll talk about in additional element however the IPO of Strong Entertainment, talks of an upcoming IPO of Firefly, extra readability round InexperiencedFirst, and so forth. are all constructive tendencies.

At the 2021 BTN shareholder assembly in Charlotte, I believed Kyle and the BTN workforce laid out a pleasant presentation and Q&A session that helped unravel a few of the complicated construction.

To bounce again to John Malone, he has tried to lower the complexity of his investments by creating monitoring shares from his TCI empire within the Nineteen Eighties-90s. “Malone’s tracking stocks increase transparency allowing investors to value parts of the company that have previously been obscured by TCI’s byzantine structure.” Is the same pattern occurring at BTN the place administration will unwind the valuation complexity?

Furthermore, I perceive how the complexity and interrelated investments may lead individuals to assume some bills are being coated up or misallocated. As already stated, it could make buyers squirrely. But FGI is the most important shareholders in BTN, FGF, BTKI with vital positions in InexperiencedFirst, OppFi, and Hagerty. I don’t see how there can be a big web profit for FGI in shifting bills or investments from one pocket to the opposite particularly contemplating FGI is non-fee based mostly.

It seems from their most up-to-date ADV that FGI’s AUM is round $125m. Kyle has publicly said a number of occasions not too long ago that FGI’s invested capital is nearly all from Joe Moglia, Kyle and their households (there seems to be 15 whole buyers in FGI). To reiterate, Kyle has said that FGI now not prices their buyers charges. All of Kyle’s web price other than money, his home and a fishing boat is in corporations throughout the BTN complicated, besides technically BK Technologies which nonetheless has investments in BTN complicated corporations.

I’ll let the reader determine whether or not they really feel aligned with administration, however it appears the one approach Kyle and FGI make or lose cash is that if the BTN complicated fairness worth will increase or decreases.

Costs

One of the principle causes for holding firm reductions in public markets is the unallocated overhead prices that it takes to run the holding firm. Often occasions, the holding firm trades under its web asset worth (“NAV”) as a result of the investor can be higher off personally shopping for the entire corporations throughout the holding firm ,if they’re public, to keep away from overhead prices and extra taxation.

This low cost could be offset by a premium for the capital allocation expertise of the holding firm’s managers and the power of the holding firm to entry investments the typical investor couldn’t.

The FY 2020 unallocated overhead prices for BTN have been ~$6.5m and must be within the $4.5m-$5.0m vary for FY 2021. This has come down from ~$8.0m when Kyle and FGI took over, however it nonetheless seems there may be room for overhead prices to lower additional.

I used to be going to investigate different holding corporations to see what the typical overhead prices have been as a p.c of sure metrics (property, market cap, and so forth.) however that turned out to be tough to do on a like for like foundation.

Maybe that is an unfair comparability but when BTN was a hedge fund construction, we might be paying them $1.5m-$2.0m underneath a 2/20 arrange. There aren’t any precise numbers on the market, however it seems there may be not less than $1.5m to $2.0m further prices for a public firm versus a personal firm so we in all probability must issue that in to the hedge fund comparability.

To once more be that man that quotes The Outsiders, “The Edifice Complex…there is an apparent inverse correlation between the construction of elaborate new headquarter buildings and investor returns.” Not one of many CEOs talked about in The Outsiders constructed lavish headquarters or had pointless overhead prices.

When Kyle and FGI went activist at BTN they said the significance of reducing prices and I hope it continues to be a key issue going ahead. We will additional tackle this within the inflection level part, however I’m referring to chopping pointless overhead prices related to redundant holding firm operations. I’m not suggesting chopping prices by underpaying administration or not investing in progress.

The largest draw back to pointless overhead prices is that it makes time the enemy for BTN shareholders. The longer it takes for the market to comprehend the undervaluation of BTN, the extra the overhead prices have decreased the fairness worth.

This goes to begin sounding repetitive however on the present valuation of BTN it doesn’t matter if administration lowers the present unallocated overhead prices. It appears possible buyers would nonetheless get the present market cap again even when overhead prices stay the identical and a draw back situation happens in all 5 BTN property.

Ballantyne Strong’s Five Assets

1. 100% possession in Strong Entertainment

The undervaluation of Strong Entertainment might be probably the most integral a part of the draw back safety piece ,tails we don’t lose a lot, of BTN’s fairness valuation.

Strong Entertainment manufactures and sells film theatre screens in addition to gives upkeep and repair to beforehand bought screens. The North American and European film display screen business is principally a duopoly between Strong Entertainment and Harkness. Strong Entertainment dominates North America and Harkness, based mostly in Ireland, dominates Europe. Additionally, Strong Entertainment is the unique provider for Cinemark (~5900 screens) and IMAX (~1650 screens).

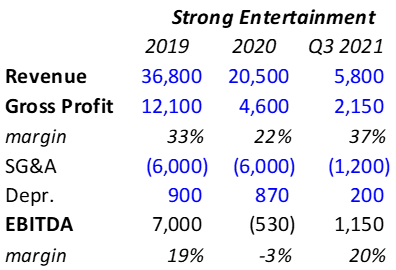

Needless to say, the pandemic hit Strong Entertainment arduous. In 2019, Strong Entertainment had ~$37m in gross sales and in 2020 they’d ~$21m in gross sales.

2020 BTN 10k & Q3 2021 10Q

As seen above, not solely did income collapse in 2020 however margins collapsed as properly. The margins compressed in 2020 partially because of fastened prices within the enterprise but in addition as a result of Strong Entertainment was absolutely geared as much as have one other $35+m income 12 months and was caught off guard like the remainder of the world. I suppose that’s fastened prices as properly however, for my part, extra one-off fastened prices.

The motive Q3 2021 is embrace above is:

a) I’d say that Q3 2021 is probably the most “normal” quarter we’ve had in nearly two years

b) To present that administration has discovered a option to get again to 18%-20% EBITDA margins regardless of not being again to an over $35m income run price.

This might be extrapolating an excessive amount of out of only one quarter of outcomes, however it’s definitely a constructive pattern.

We may additional spotlight the upside potential of the worth of the 100-year-old “Strong” model identify, their proprietary display screen coating, the pivot to promoting screens to colleges, theme parks, concert events, museums, and so forth. But it’s necessary for our draw back safety theme to concentrate on the truth that administration appears to have adjusted to the “new normal.” Strong leisure administration has stabilized margins and been in a position to run a worthwhile ,though fairly lower than in 2019, enterprise.

This signifies that if the film business does return or one other sector begins to persistently purchase film screens, Strong leisure could have the capability at their warehouse in Quebec to ramp up once more to over $35m in income with none progress capex ,moreover working capital,….heads we win.

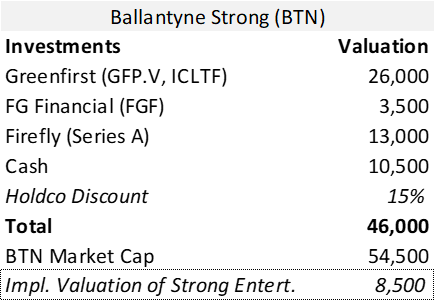

As administration has famous, BTN plans to IPO Strong Entertainment this 12 months. As seen within the sum of elements, the market seems to be ascribing a $0-$10m fairness valuation for the Strong Entertainment IPO.

Maybe the market thinks that Q3 2021 was a one-off and Strong Entertainment can be burdened by fastened prices and burn money until they return to $35+m income, perhaps they’re nervous concerning the over reliance on IMAX and Cinemark, perhaps they see one thing I’m completely lacking.

I don’t know however as seen under utilizing conservative projections based mostly off of Q3 2021 numbers an fairness valuation of $0-$10m appears unlikely.

Excel

We didn’t get into the nuisances of film display screen gross sales income versus servicing already bought screens and what number of film theatres have been laying aside servicing their screens over the previous two years. But let’s simply preserve the draw back valuation excessive degree and if we wish the closest public market comp when making an attempt to determine an fairness valuation for Strong Entertainment, take a look at Moving iMage Technologies (MITQ).

Despite the draw back safety theme, if Strong Entertainment is ready to get again to 2019 EBITDA ranges of ~$7m the “head I win” is important.

Another extra qualitative upside potential for Strong Entertainment following the IPO is a renewed entrepreneurial spirit. Having Strong Entertainment be their very own firm and their outcomes now not being blended in with the remainder of the BTN corporations’ outcomes signifies that the Strong Entertainment managers can be correctly compensated and incentivized for the person efficiency of their enterprise. This ought to additional energize Strong Entertainment administration to develop the enterprise and improve profitability.

2. ~8.6% possession in InexperiencedFirst Forest Products

Rick Doman (CEO); Paul Rivett (Board Chair); Larry Swets (Board member)

InexperiencedFirst Forest Products is a publicly traded lumber mill firm that was began although buying seven lumber mills in Eastern Canada, six of the seven from Rayonier, with an annual manufacturing capability of ~905 MMFbm (prime ten in Canada).

As I’m penning this, lumber costs are skyrocketing to above $1100 per thousand board toes for the second time this 12 months. InexperiencedFirst’s market cap is slowly rising however I’d assume at these lumber costs InexperiencedFirst is producing 50+% free money circulate to fairness yields.

Furthermore, administration at InexperiencedFirst is very skilled with Rick Doman as CEO, whose household has been within the Canadian lumber business for generations, and he personally based EACOM timber, and Paul Rivett as Board Chairman, who was president of Fairfax Financial.

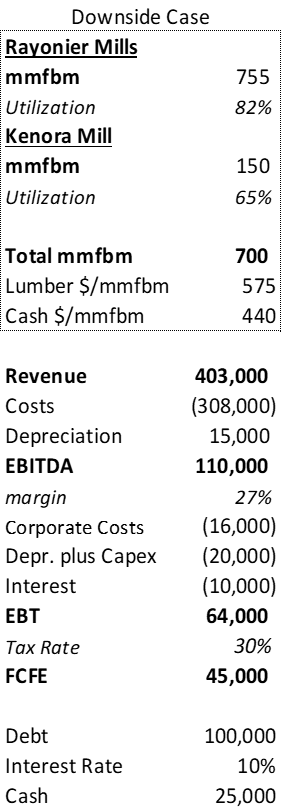

The property they acquired nevertheless usually are not prime notch as previous to InexperiencedFirst buying the six Rayonier lumber mills they might solely run at a low 80% utilization price and are nonetheless in want of serious capex enhancements. The Kenora lumber mill was mothballed earlier than it was purchased.

The Company has laid out a plan to spend $50+m of capex to decrease money prices and improve capability/utilization. This is after they pay down or refinance their $100m debt with a ten% rate of interest which ought to have not too long ago been made lots simpler with lumber costs skyrocketing once more.

Even if none of that is applied and lumber costs normalize at $575 per thousand board foot ,50+% under at present’s costs, utilizing conservative assumptions a ~$45m of free money circulate must be achievable which is 15+% free money circulate to fairness yield on the present ~$290m InexperiencedFirst market cap.

Excel

All of the above values are in USD. Raised money prices to replicate doubling in Canadian tariffs

A deeper dive evaluation not executed by me is offered right here

Additionally, an enormous a part of the InexperiencedFirst thesis was that Canadian lumber manufacturing would slowly transfer away from western Canada and into japanese Canada. This has begun to be validated as Interfor and Canfor have not too long ago purchased related measurement lumber mill capacities as InexperiencedFirst in japanese Canada for 2-3x the value InexperiencedFirst paid for his or her Rayonier property. That being stated, the lumber mills not too long ago acquired are in all probability of upper high quality.

On a aspect be aware, Interfor acquired EACOM which was based by InexperiencedFirst’s CEO Rick Doman.

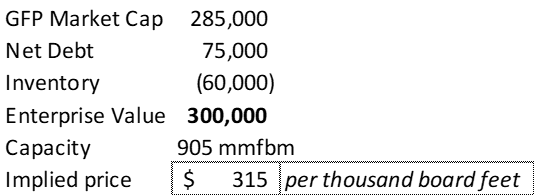

I’m no knowledgeable within the nuisances of the lumber business however from a previous profession I do know that valuing a commodity enterprise off of money circulate in all probability isn’t the very best metric. Although this turns into considerably round, when you see the numbers under the market is implying a valuation of ~$300-$320 per thousand board toes for InexperiencedFirst’s lumber mills

Excel

At this level I’m approach over my skies in speaking about lumber business valuations, however I really feel snug saying that InexperiencedFirst is buying and selling at or under alternative value contemplating the entire latest Canadian lumber mill transactions have been above $450+ per thousand board toes.

As talked about, these InexperiencedFirst property are subpar so perhaps a reduction is warranted however this additionally isn’t factoring the upside of: the paper mill, the secured lumber provide, the opportunity of monetizing land across the lumber mills, the skilled administration workforce and the macroeconomic tailwind.

Under a draw back situation, we’ve got sub-par japanese Canadian mills run by prime tier administration. Even when you assume lumber craters, underneath nearly each situation the chance appears possible that fairness buyers would not less than get the present market cap again. This provides InexperiencedFirst fairness buyers a free embedded name possibility on lumber costs staying considerably elevated for a number of years.

Credit to Mike Mitchell (now InexperiencedFirst and BTN board member) for introducing me and a number of the worth investing world to InexperiencedFirst

3. ~20% possession in FG Financial

Larry Swets (CEO); Kyle Cerminara (Board Chair)

FG Financial began as an insurance coverage firm underneath the identify 1347 Property Insurance Holdings (PIH) which IPO’d in 2014. Before the IPO, PIH was a subsidiary of Kingsway Financial Services (KSF) the place Larry Swets was CEO till 2018.

PIH wrote P&C insurance coverage in three southern states till promoting their insurance coverage companies to FedNat Holding Company (FNHC) in 2019 for $51m ,50% money and 50% inventory. In 2020, PIH modified its’ identify to FG Financial and outlined their new technique as “focus on opportunistic collateralized and loss capped reinsurance while allocating capital to SPACs and SPAC sponsor-related business.”

Since 2020, FGF has sponsored two SPACs ,particulars under, which have resulted in investments in OppFi (OPFI) and Hagerty (HGTY). FGF CEO, Larry Swets, has alluded to the truth that he feels FGF has discovered a distinct segment in sponsoring $100m- $250m SPACs that put money into Fintech and InsureTech corporations with enterprise values between $500m and $2b.

FGF can be constructing a SPAC platform that can assist advise different SPAC sponsors on their fundraising in addition to providing ancillary providers corresponding to D&O insurance coverage.

Right now, FGF consists of 4 main property

- ~8% possession in FedNat (FNHC): P&C Insurance firm

- ~1.4m shares: ~$2.0m valuation

- Limited in what number of shares they’ll promote till 2024

- <1% possession in OppFi: Fintech platform for lending to sub-prime shoppers. FGF’s first SPAC funding

- 860k shares: ~$5.2m valuation

- 360k warrants @ $11.50 strike: ~$400k valuation

- <1% possession in Hagerty: Insurance underwriter for traditional car. FGF’s second SPAC funding

- 533k shares: ~$8.6m valuation

- 321k warrants @ $15 strike: ~$400k valuation

- Reinsurance portfolio, SPAC division/platform, and different investments

- Book Value of Reinsurance: ~$2m

- Other Investments: Valuation of ~$6-7m (not too long ago bought REIT)

- Implied Valuation of SPAC division/platform: ~$15-16m

Considering three of the 4 main property in FGF are publicly traded the one actual significant implied valuation is their SPAC division/platform:

It is fairly easy to see the upside potential within the SPAC division/platform. Having the power to instantly put money into founder shares is a novel alternative for many retail buyers. Through the primary two SPACs, FGF has put up ~$5m for founder shares/warrants that are actually price over $15m even with Oppfi being down over 40%. I’m removed from an knowledgeable on SPACs however there may be actual draw back danger in founder shares in addition to you’ll be able to lose all of your upfront cash if a deal doesn’t undergo (nonetheless a really engaging danger/reward for my part).

As seen within the chart under, the market is implying a valuation of $15m-$16m for the SPAC division/ platform.

FGF 2020 10k

I attempted to search out the only option to worth FGF. Hopefully it makes some sense. As seen above, by utilizing the market or e book worth of all of FGF’s property alongside a reduction for holding firm overhead bills, the implied valuation of the SPAC division/platform is between $15-$16m, relying on the holding firm low cost and the reinsurance/ different investments valuation.

Despite me annoyingly reiterating the theme of draw back safety, at FGF I don’t see a lot. Almost the entire fairness worth of FGF is predicated on the long run success of their SPAC division/platform.

FGF has executed two SPAC offers in 2020-2021 and anticipates doing a mean of two to 4 yearly going ahead (some years will in all probability be zero and a few 4). Worth noting is that over $4m of most popular fairness was not too long ago raised so FGF can put money into their subsequent SPAC.

If FGF Management is ready to make investments $3-$5m into profitable SPAC sponsor shares on common 2-4 occasions per 12 months whereas additionally creating a SPAC platform for D&O insurance coverage and ancillary charges, the long run fairness worth of FGF can be many multiples of the present market cap. If the long run SPAC division/platform fails or turns into unprofitable then the present fairness valuation of FGF will seem too excessive in hindsight.

In their first SPAC, FGF and their co-sponsors have been in a position to increase a $225m SPAC with ~$90m after redemptions being invested into Oppfi to associate alongside the Schwartz household.

Their second SPAC, FGF and their co-sponsors have been in a position to increase $115m with ~$85m after redemptions being invested into Hagerty to associate alongside the Hagerty household. Additionally, a $704m non-public funding was made into HGTY on the identical time with companions together with State Farm and Markel.

Their first two SPACs present that FGF thus far is investing into properly revered, household run corporations. On prime of that, anytime a reputation like State Farm or Markel is within the record of co-investors it makes me really feel extra snug concerning the status of the SPAC workforce.

This could also be a false consolation as FGF is simply investing $1-$5m in every of those SPACs and have lower than 1% possession in every. So maybe the Schwartz/Hagerty household, State Farm, and Markel don’t care about FGF’s status since FGF’s possession is so small, however you must really feel this not less than begins to offer legitimacy to FGF’s SPAC division/platform.

Finally, it seems that FGF has already upgraded the businesses they’re investing in from their first SPAC to their second SPAC. The jury continues to be out on Oppfi however the inventory worth has gone down over 40% since de-SPACing and there was only a CEO change. It nonetheless feels like an progressive enterprise with large upside potential however in want of some hands-on work. Whereas from all the pieces I’ve heard and skim Hagerty is an A+ enterprise that’s on cruise management.

This is a long-winded approach of claiming that it appears cheap to ascribe not less than a $15m-$16m valuation to the way forward for the SPAC division/platform. Just take into account that FGF’s first two SPAC investments inside a 12 months have generated over $15m in fairness by investing $5m of capital.

Admittedly, FGF breaks the theme of draw back safety however I hope I did an honest job at highlighting the upside potential.

4. $13m Preferred Shares in Firefly

Kaan Gunay (CEO); Kyle Cerminara (Board member)

Firefly is a privately held, VC backed outside promoting firm that was launched in 2017. They personal and function the good digital screens on prime of taxis/rideshare automobiles in main US cities corresponding to LA, San Francisco, Chicago, Miami, Las Vegas, New York and are at present increasing into Boston, Atlanta, Austin, Dallas and Philadelphia amongst many extra cities to come back in 2022.

The enterprise is extra refined than at first look because the digital promoting display screen on prime of the automobiles is linked to the web which permits the advertisers to focus on their viewers based mostly on the situation of the car, time of day, climate, and different necessary variables.

Firefly operates a two-sided app market between drivers and advertisers the place taxi/rideshare drivers can earn further revenue ,a mean of $300-$400/month in 2019, whereas advertisers can show their advertisements in focused areas in a matter of seconds.

When BTN’s administration workforce was constructing Strong Outdoor, an organization that bought digital screens to placed on prime of Taxi Cabs, they took discover of Firefly whom they have been competing towards particularly in New York City. BTN determined that as a substitute of competing with Firefly they might relatively associate alongside them.

BTN bought their Strong Outdoor property ,300 digital screens that have been spun out of Convergent (extra on this in subsequent part), to Firefly in 2019-2020 in change for ~$9m of most popular shares. BTN moreover invested $4m money in Firefly in 2020 and now owns ~$13m of most popular shares in Firefly.

Of the $13m BTN holds roughly:

- $5.7m price of Preferred Series A-2 shares

- $7.4m price of Preferred Series A-3 shares

According to a couple sources the A-3 pre-money valuation was ~$150-$200m (apparently ~10x income). I consider collection A-2 could have been on the decrease vary of $150-$200m however I don’t have any confirmed data on the valuation. All of this data could possibly be completely flawed as none of it has been made formally public. Of be aware, different main buyers within the A-3 most popular shares have been Google Ventures, NFX, and Endeavor Catalyst.

Over the previous 12 months, Firefly has raised cash in a collection B spherical ,at apparently $300m pre-money valuation, and is now fundraising for collection C.

In June 2021, Firefly acquired their main competitor Curb Taxi Media which now provides the mix enterprise entry to over 10,000 digital screens in 11+ main cities.

From the studies coming from BTN administration ,Kyle is on the Firefly board, it feels like Firefly is on the quick observe for an IPO within the subsequent 12 months or two.

After Series B and Series C rounds, I do not know what proportion of Firefly BTN now owns however I really feel snug that’s price fairly a bit extra ($17-20+m) than the $13m on the steadiness sheet however our draw back case will assume $13m. It has been requested on quarterly calls and administration has not disclosed the p.c possession.

There are nonetheless some particular headwinds for Firefly as Uber and Lyft have not too long ago develop into rivals, the rules round cities permitting the digital screens continues to be a gray space and it’s unclear how a lot further capital can be wanted for Firefly to get to scale. Still in nearly each situation the chance appears very possible that BTN will get not less than $13m again from their Firefly funding.

Lastly, the upside potential of Firefly is important. There are positively potential community results as every taxi/rideshare driver downloads the Firefly app to see how a lot further revenue they’re incomes or may earn and every media firm downloads the app to purchase their promoting area on the digital screens. The extra taxi/rideshare drivers that use the app the extra worthwhile the app turns into to advertisers and the extra advertisers utilizing the app the extra money the taxi/rideshare drivers make.

Can you think about an commercial of the Knicks warming up dwell earlier than a basketball sport in Madison Square Garden that’s placed on each taxi/rideshare digital display screen inside a 30 block radius of MSG to remind individuals to purchase final minute tickets? Tails we get our $13m again, Heads we may get the complete present market cap of BTN.

5. $10.5m money

Nothing actually so as to add right here however I’ll depart it as much as the reader to prognosis how a lot $10.5m in money is price within the palms of BTN administration.

A fast be aware, in 2019 BTN began a expertise incubator that homes ~40 start-up corporations of their co-working facility in Alpharetta, Georgia known as Digital Ignition. I’ve not factored this into the valuation of BTN.

How BTN acquired possession in every Equity Investment

1. Itasca Capital turns into InexperiencedFirst Forest Products: The Good Investment So Far

Before BTN invested in Itasca Capital in 2016, Itasca Capital was known as Kobex Capital Corp (KXM), a Canadian mineral and exploration firm. Kingsway Financial Services, whose CEO was Larry Swets till 2018, made a hostile takeover of Kobex in 2015 the place they liquidated all of their mineral and exploration property and altered the identify to Itasca Capital. Larry turned CEO of Itasca Capital and Kyle was a director.

It will get complicated.

Once KFS was answerable for Itasca Capital, they invested the money from the Kobex liquidation, ~$10m, into 1347 LLC which was the SPAC sponsor alongside KFS that took Limbach Holdings (LMB) public. LMB designs, installs and maintains HVAC and plumbing methods.

Within 1347 LLC, there have been 400k most popular shares in LMB, ~2.8 million widespread shares of LMB, ~200k warrants in LMB at a strike worth of $11.5 and ~500k warrants in LMB at a strike worth of $15.0.

To additional complicate this, Itasca Capital’s $10m invested in 1347 LLC was a novel arrange.

Itasca Capital purchased the entire $10m of most popular redeemable class A shares in 1347 LLC that carried a 1%/month rate of interest after which paid 44.44% of the remaining revenue after the popular claims of shares B,C,D have been paid. The Class A shares represented ~47% of the voting curiosity of 1347 LLC.

In May via December 2016, BTN invested $3.7m ,~32% possession, in Itasca Capital.

If you’re in some way nonetheless following alongside, in September 2019, Itasca Capital redeemed their funding of their Class A most popular shares in 1347 LLC for $9m in money and shares in LMB price ~$300k. Of be aware, Itasca Capital had already been paid $4m in money from 1347 LLC earlier than the redemption in 2019.

In October 2020, Itasca Capital used the 1347 LLC $10m proceeds to purchase one sawmill in Kenora, Ontario and on the identical time raised ~$4m collectively from Rick Doman and Paul Rivett.

Then in August 2021, Itasca Capital, which by now had modified its identify to InexperiencedFirst, acquired six sawmills in Eastern Canada for ~$240m ,together with ~$80m of stock, by elevating fairness and debt.

The level of penning this intimately is to not give the reader a headache ,which I’m certain it did, however to point out how BTN’s administration turned a $3.7m funding in 2016 right into a profitable funding in InexperiencedFirst price $13-15m (dividends included) by 2021.

BTN administration invested a further $8.3m in InexperiencedFirst in 2021.

The funding highway to ultimately get to InexperiencedFirst was extremely bumpy and sophisticated alongside the way in which. The market worth of BTN’s authentic $3.7m funding had gotten right down to ~$1m not together with dividends. In 2018, when you have been a BTN shareholder you in all probability weren’t completely satisfied in any respect with the Itasca Capital funding. It was down nearly 60% and also you have been in all probability questioning the entire complexity and interrelated social gathering transactions . Now the $3.7m has become what seems to be a terrific funding going ahead.

2. FG Financial: The Bad Investment thus far

As briefly mentioned, BTN administration invested $7.7m in 1347 Property Insurance Holdings (PIH), not the identical as 1347 LLC, from 2016-2017. At the time of the funding, PIH was run by Larry Swets and operated as a P&C insurer primarily in Louisiana, Florida, and Texas.

In 2019, PIH bought their operations to FedNat Holding Company for $51m which was paid 50% in money and 50% in inventory of FNHC. The major capital allocation mistake was not taking the payout in all money or a subordinated be aware, even when it will have been much less. The 50% inventory of FNHC was initially price $25.5m on the time of the deal and is now price ~$2.0m.

PIH modified their identify to FG Financial in 2020 and have used the $25.5m money portion from the FedNat insurance coverage sale to take a position $5m in Oppfi/Hagerty founder shares and likewise put money into writing reinsurance, share buybacks, constructing a SPAC platform and some small investments. FGF nonetheless has $10+m remaining in money after the REIT funding sale.

Although the allocation of the $25.5m in money has produced sufficient returns thus far, dropping over $23m within the valuation of FNHC inventory has prompted BTN’s authentic funding of $7.7m in 2016-2017 to now be price ~$3.5m

3. Firefly: Turning Convergent Media Around

In 2013, BTN’s former administration ,earlier than Kyle and FGI took over, acquired Convergent Media, an outside promoting firm, from Sony for ~$17m. At the time of acquisition, Convergent had ~$40m in gross sales. By 2014-2015, the income dropped to $17m and Convergent was dropping cash. As already mentioned, Kyle and FGI determined they wanted to go activist at BTN after the worth destroying Convergent acquisition.

In 2018, Kyle and BTN administration spun off Strong Outdoor from Convergent. Strong Outdoor used 300 “smart” digital screens alongside non-digital taxi prime shows to put ads on 3,500 cabs in New York. In 2020, BTN administration bought Strong Outdoor to their competitor Firefly in change for $9m price of Series A shares and later invested $4m in additional Firefly Series A shares.

Additionally in 2021, BTN bought the remainder of Convergent for ~$17m fairness valuation ($23m Enterprise Value). Although it took a number of years Kyle and the BTN administration have been in a position to flip a collapsing Convergent enterprise into $9m of the $13m funding in Firefly and ~$17m in money which has been used to take a position ~$8.3m in InexperiencedFirst and the remaining continues to be money on the BTN steadiness sheet.

If you have an interest in additional capital allocation tales take a look at Kyle’s investments through Fundamental Global in Iteris (ITI), Magnatek (MAG) and persevering with funding in BK Technologies (BTKI) to call a number of.

Conclusion (The Inflection Point)

It is my opinion that BTN alongside Kyle and Larry appear to be going via an inflection level. When Kyle first began investing in 2012 via FGI, he gave the impression to be a cigar butt investor that went into tremendous low cost corporations and squeezed out that final little bit of worth via activist investing. This could be seen with FGI’s funding in BTN in 2015 as the corporate was low cost however wanted a ton of hands-on work.

Especially over the past 12 months or two, Kyle and Larry appear to be viewing themselves now extra as capital allocators as a substitute of operators and their major job being to search out distinctive methods to obtain capital inflows to allow them to make investments into companies and administration groups they deem as prime quality.

Some of this inflection level was made clear simply by simply studying the tea leaves of their latest investments however proper as I used to be ending this write up Kyle went on Microcap Investing podcast and confirmed a number of these mindset shifts which have led to this funding method change.

Kyle principally stated that he now not views aggressive activism as obligatory, he would relatively simply fund an organization from the bottom up with a superb administration workforce than go activist right into a microcap firm to show issues round as he did at BTN and Itasca Capital (with Larry) amongst others. Additionally, he stated he needs to be on much less boards sooner or later and that he has transitioned from a Graham and Dodd investor ,cigar butt, to investing in good administration groups at truthful costs.

This funding change isn’t revolutionary as it’s the identical path that Warren Buffet and will different well-known worth buyers have gone via. But it does appear to be coming to fruition in BTN’s most up-to-date investments

Just a few examples that come to thoughts are partnering with Rick and Paul in InexperiencedFirst, teaming up with Firefly as a substitute of competing towards them, investing alongside the Schwartz/Hagerty household in FGF, giving the CEO function of BTN to Mark Roberson, and Kyle giving his InexperiencedFirst board seat to Mike Mitchell.

Another inflection level I see unfolding is Kyle and Larry investing in bigger corporations. The first tea leaf right here for me was once they invested in InexperiencedFirst adopted shortly by Oppfi and Hagerty. Kyle and Larry noticed the standard of administration and board chair/members you’ll be able to appeal to when you’ll be able to pay them a better wage and embrace inventory bonuses with actual upside potential. Kyle goes into this in some element on the Microcap Investing podcast talked about.

The query BTN buyers must ask themselves is what does this inflection level imply for BTN after the Strong Entertainment IPO? BTN administration has stated they plan on sustaining a majority curiosity in Strong Entertainment after the IPO however what is going to BTN administration’s subsequent transfer be after they’ve appeared to alter their mindset in the direction of viewing small microcap corporations as sub-optimal?

Will administration attempt to construct BTN into a bigger firm as they did at InexperiencedFirst? Or will they go the wrong way and liquidate the remaining BTN investments after the Strong Entertainment IPO (particularly if Firefly IPOs quickly)?

If BTN administration decides to develop as a substitute of liquidating all indicators level to reducing pointless overhead prices, lowering complexity, and a brand new discovered capital allocation methodology of investing in stable administration groups. This inflection level will hopefully slowly begin to appeal to a stable, long-term shareholder base. But to stay with the theme, none of this must occur for buyers to get the present market cap again and even when a few of it does…heads we win.

Valuation

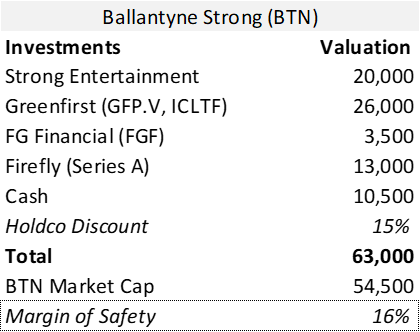

Downside Scenario: Sum of Parts

Excel

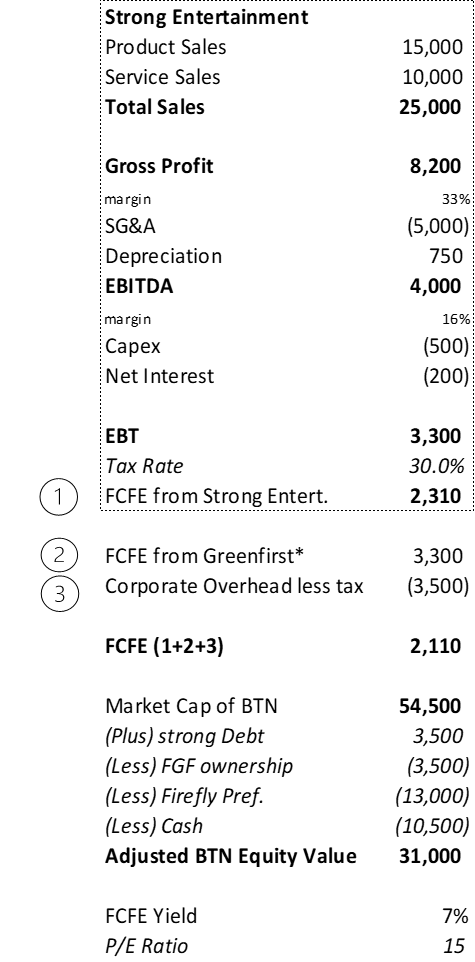

Downside Scenario: Cash Flow

Excel

*displays tax inefficiency of distributing earnings from InexperiencedFirst

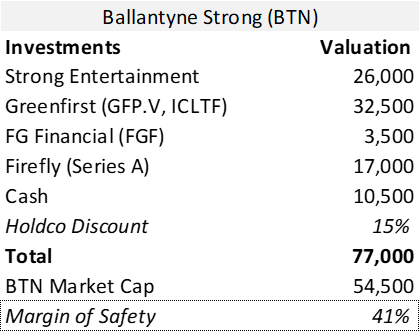

Base Case Scenario: Sum of Parts

Excel

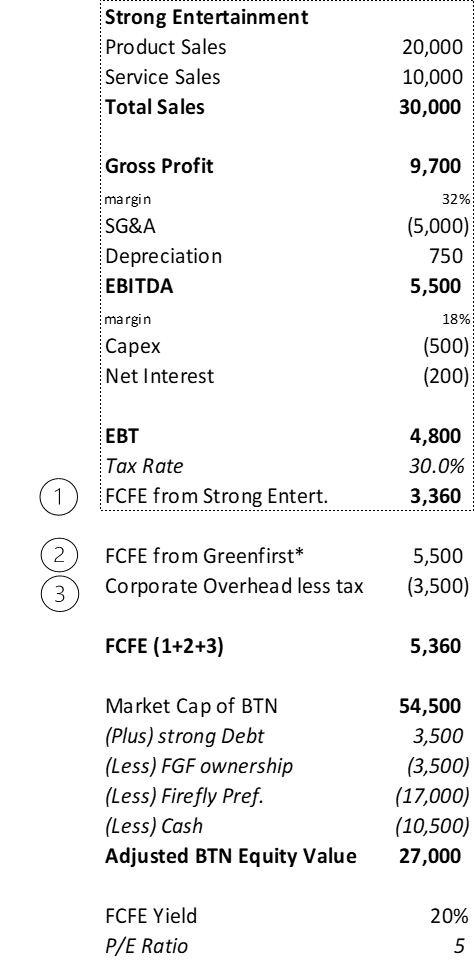

Base Case Scenario: Cash Flow

Excel

*displays tax inefficiency of distributing earnings from InexperiencedFirst

“The function of the margin of security is to render the forecast pointless”- Ben Graham

Recommendation

First off, apologies for the way lengthy and repetitive at occasions the write up is. It was one of the best ways for me personally to scale back the complexity of valuing BTN.

After studying the write up when you really feel an inflection level in BTN is underway, I recommend making an attempt to make an knowledgeable choice on whether or not or to not put money into BTN earlier than the Strong Entertainment IPO, we must always get extra particulars on the precise date earlier than or through the upcoming quarterly convention name, which very properly could possibly be the catalyst for lowering the complexity of valuing BTN and buyers higher understanding BTN’s new capital allocation technique.

Appendix

Catalysts

- Strong Entertainment IPO

- Firefly IPO

- InexperiencedFirst up-listing

- FGF Announced SPAC

- BTN invests their $10.5m in money right into a stable funding

Risks

Companies have doubtlessly depressed market costs for 3 causes:

- High danger, low uncertainty

- High danger, excessive uncertainty

- Low danger, excessive uncertainty

Fourth on this record is low danger, low uncertainty which might be companies that are pretty priced with common danger/return traits (a regulated utility firm can be an instance).

A spinoff of this framework of enthusiastic about danger is Richard Zeckhauser’s Unknown and Unknowable.

Due to BTN’s present market cap, I’d classify BTN fairness as low danger, excessive uncertainty

Some of areas of excessive uncertainty embrace:

- How to worth BTN

- Relationship between a personal funding fund being the most important shareholder in a microcap firm

- Declining theatre business

- Large drop in lumber costs or one other large improve in Canadian lumber tariffs

- Firefly rising too quick and needing to boost dilutive capital (under Series A valuation)

- Investments in SPACs cease utterly or market turns into far more environment friendly

- What BTN’s subsequent transfer is as soon as they IPO Strong Entertainment

To proceed to beat a lifeless horse, even when the draw back case situation occurs in the entire areas of uncertainty it’s possible BTN buyers will get the present market cap again which is why I classify it as low danger, excessive uncertainty.