Klaus Vedfelt/DigitalVision by way of Getty Images

Shares of Harley Davidson Inc. (HOG) have returned about 2% since I put out my bullish piece on the corporate towards a achieve of ~70% for the S&P 500. This slightly huge underperformance has me intrigued, so I believed I’d test on the identify to see if it is smart so as to add to my small place. I’ll make this dedication by a number of the highlights (and lowlights) of the monetary historical past right here. I wish to deal with the query of dividend sustainability. Also, I wish to take a look at the inventory as a factor distinct from the underlying enterprise. Also, as my common readers may guess, I’m going to put in writing about potential alternatives with brief put choices right here.

My Prejudices and A Quick Note On Livewire

Before moving into the article, I’ll come clean with my prejudices up entrance. I experience a Triumph bike, and have associates who experience Hondas, BMW, Indians, and I even knew a man who rode a Royal Enfield. I’ve additionally acquired some associates who experience Harleys, although I do not know why. I’ve check pushed Harleys a number of occasions and customarily preferred the bikes themselves. While I like a few of their bikes, for my part (and I’m actually not alone on this view), there’s one thing a bit off about “Harley Culture.” Only a choose variety of them wave to fellow motorcyclists, they appear to have a way that “there are two types of bike on the road: Harleys and scooters” (that’s a direct quote that was barked at me by a Harley rider). Perhaps it’s a results of my excessive type of republicanism, however I don’t take care of snobbery of any form.

Now, I’m as a lot of a fan of lengthy gray pony tails and mama denims flapping within the wind as the following man. The factor is once I suppose “Harley Culture” now, I believe “beer gut”, “Fog Hat”, “belching loudly because some oaf thinks it’s funny.” While I can admire the truth that these bikes are far more technologically subtle than is mostly believed, I can’t see myself shopping for one as a result of I don’t wish to be related to a tradition that’s so embarrassingly, un-self consciously uncool. Just as a result of I’ve some sturdy views concerning the product doesn’t imply I’m not open to proudly owning the enterprise on the proper value, although.

In spite of the truth that the Livewire model has made the information in monetary markets, we should always do not forget that as of very lately, the electrical bike goes to be carried by solely about 12 dealerships. That represents ~1.7% of sellers within the United States, and about .8% of sellers globally. The SPAC is thrilling, however I don’t suppose the monetary impression of the spinoff is critical a method or one other, so I’ll not touch upon Livewire particularly. I believe the irrelevance of the deal is pushed residence by the truth that shares have languished because it was introduced.

Thesis Statement

I think about you’re a busy crowd, expensive readers. You’ve acquired a freeway to get below your wheels, and also you subsequently have restricted time to learn my tangled screeds. For that motive, I’ll give you my ideas on this identify on this, the “thesis statement” paragraph. I’ll write all of this out simply in case you one way or the other discovered your self at this fifth paragraph, having shot proper previous each the title, and the abstract bullet factors above. If you’re not a fan of spoilers, and wish to uncover the magical treasures of my narrative as they emerge, I’d suggest skipping this paragraph. If you’re nonetheless right here, I’m assuming you’re comfortable with me wrecking the shock. You’ve been warned, so don’t whine like a Harley rider whose man-bra lastly offers out about spoiling the thrill. The reality is that I’m not holding out hope for a lot progress at Harley Davidson, and I believe the inventory will commerce off the dividend consequently. The proven fact that the dividend is sustainable for my part is subsequently critically vital. I additionally suppose (although haven’t any proof to imagine) that the dividend will likely be returned to pre-pandemic ranges over the approaching years. Given the relative significance of the dividend right here, this is able to be very supportive of the inventory value. Most vital of all, although, is my view that the shares are buying and selling at a really pessimistic degree. I like to purchase low-cost, and the mix of sustainable dividend at ridiculously low-cost valuations could be very compelling. In addition, I’ll be promoting some places that generate ~6.6% on funding capital.

I believe it’s affordable to counsel that Harley’s a money cow, in gentle of the truth that income progress has been mainly non-existent for the previous a number of years. This is comprehensible in gentle of what’s occurred to bike demand over the previous a number of years.

The firm has additionally managed to take care of profitability over the previous a number of years, even throughout the interval of the pandemic, which is kind of the feat for my part. The proven fact that administration has returned just below $6 billion of capital to homeowners since 2013 is a blended blessing in my view. On the one hand, I like the truth that they’ve returned just below $1.8 billion to homeowners within the type of dividends. That’s good. They additionally spent ~$4.15 billion of proprietor capital on buybacks since 2013 and that has not labored out properly in any respect. I believe 2015 is a consultant yr. The firm spent simply over $1.5 billion on buybacks in 2015 alone. The inventory began that yr priced at ~$62. It ended the yr at ~$45. I’d counsel that if administration needs to return capital to homeowners, they’d be higher off sending dividends.

Speaking of dividends, I believe the sclerotic progress right here suggests this inventory will commerce off its money yield, and for that motive I wish to spend a while trying on the sustainability of the dividend. When I attempt to decide whether or not a dividend is sustainable or not, I take a look at the scale and timing of future money obligations, and I evaluate that to present money and certain future money. The wider the unfold between the money stream and contractual obligations, the extra sustainable the dividend.

First, right here’s a schedule of the scale and timing of the corporate’s upcoming long run debt funds. These funds characterize the only largest supply of outflows, so I believed it’d be useful to focus right here. Note the comparatively important repayments over the following few years.

The Size and Timing of Harley’s Long Term Debt Payments Harley Davidson 2020 10-Okay

Against these obligations, the corporate has money on the stability sheet of ~$2.06 billion. In addition, Harley has generated a median of $1.084 billion in money from operations over the previous three years, whereas investing a median of $412 million. All of this instructed to me that the dividend is fairly properly lined, and I believe traders might really feel safe shopping for this inventory on the proper value.

Harley Davidson Select Financial History Harley Davidson Investor Relations

The Stock

Some of you who comply with me usually know that it’s at this level within the article the place I grow to be an actual downer by writing one thing like “just because a stock sports a sustainable dividend does not make it a sound investment” or equally temper killing rhetoric. While it will not be a cheery message, the very fact is {that a} given firm is usually a nice or horrible funding relying totally on the value paid for it. I’ll drive this level residence through the use of Harley inventory for instance. Someone who purchased this in late March of 2021 is up ~3% since. Someone who purchased a month later is down ~30%. The firm didn’t change all that a lot in that month, so the 35% swing in returns comes down totally to cost paid. This is why I attempt to keep away from overpaying for a inventory, and demand on shopping for low-cost.

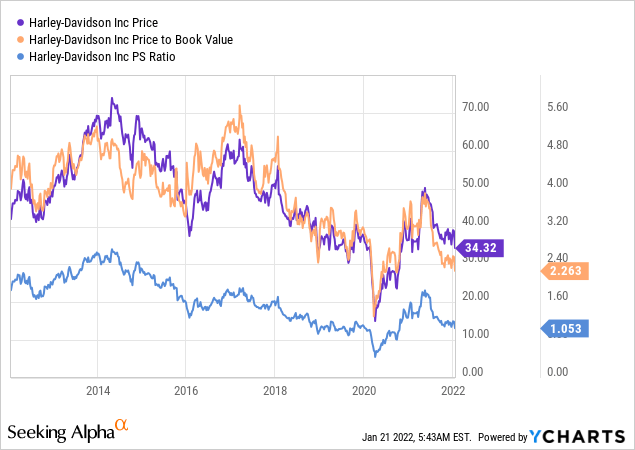

As my common reader-victims know, I measure the cheapness (or not) of a inventory in a number of methods, starting from the easy to the extra advanced. On the easy aspect, I take a look at the ratio of value to some measure of financial worth like gross sales, earnings, free money stream, and the like. Ideally, I wish to see a inventory buying and selling at a reduction to each its personal historical past and the general market. With that in thoughts, we see that the market is paying very close to a decade low for $1 of Harley Davidson’s gross sales and guide worth, per the next.

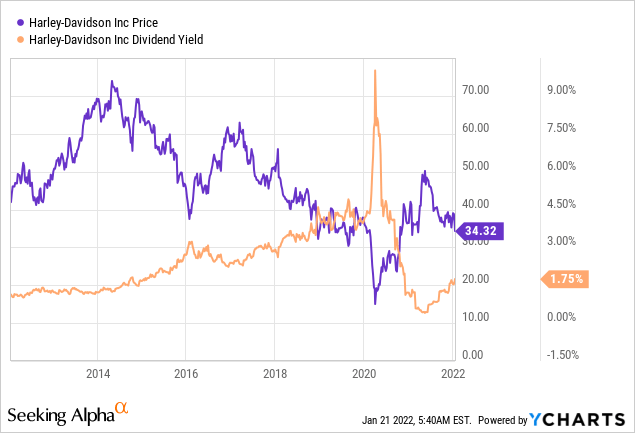

While the shares are comparatively low-cost, you could recall that I counsel that this inventory will commerce off its dividend, so we have to spend a while trying on the yield. While the yield has actually improved over the previous six months or so, it is close to a 5-year low, and is at the moment close to the 2015 lows. This low yield is a operate of the decrease dividend fee, and there is some hope (however no assure) that it will return to pre-pandemic ranges in future. I’ll anticipate proof earlier than making a name on this.

In addition to easy ratios, I wish to attempt to perceive what the market is at the moment “thinking” about the way forward for this firm. In order to do that, I flip to the work of Professor Stephen Penman and his nice guide that I can’t suggest extremely sufficient “Accounting for Value.” In this guide, Penman walks traders by how they will apply the magic of highschool algebra to an ordinary finance system as a way to work out what the market is “assuming” a few given firm’s future progress. This entails isolating the “g” (progress) variable in a reasonably normal finance system. Applying this method to Harley Davidson in the intervening time suggests the market is forecasting a progress fee of -4% for this enterprise going ahead, which I contemplate to be properly pessimistic. Given the entire above, I’ll be shopping for these shares on the present value.

But Wait, There’s More-Put Options

In addition to purchasing some extra shares, I wish to goose returns by promoting some places, as a result of I believe these are additionally an effective way to “play” this identify. In my view, brief put choices characterize a “win-win”, and they also’re too compelling to cross up for my part. I believe these are “win-win” trades as a result of the outcomes are superb regardless of the result. If the places expire nugatory, I’ll merely pocket the premium, which is nice. If the shares drop beneath the strike value, I’ll be obliged to purchase at a value that I predetermined is suitable to me, in order that’s additionally a optimistic.

At the second, I’m keen to promote the January 2023 Harley Davidson places with a strike of $25. These are at the moment bid at $1.65, which works out to a 6.6% yield on money. If the share value stays above $25, I’ll merely acquire my 6.6% return. If the shares drop 26.5% from the present degree, I’ll be obliged to purchase at a web value of ~$23.35. Holding all else fixed, that represents a 2.56% dividend yield. Being “forced” to purchase at this value can be very acceptable to me.

I hope you’re all revved up concerning the prospects of a “win-win” commerce, expensive readers, as a result of it’s time to spoil the temper by writing about threat. The actuality is that each funding comes with threat, and brief places are not any exception. We do our greatest to navigate the world by exchanging one pair of risk-reward trade-offs for one more. For instance, holding money presents the danger of abrasion of buying energy by way of inflation and the reward of preserving capital at occasions of maximum volatility. The dangers of share possession ought to be apparent to readers on this discussion board.

I believe the dangers of put choices are similar to these related to a protracted inventory place. If the shares drop in value, the stockholder loses cash, and the brief put author could also be obliged to purchase the inventory. Thus, each lengthy inventory and brief put traders usually wish to see greater inventory costs.

Puts are distinct from shares in that some put writers do not wish to really purchase the inventory – they merely wish to acquire premia. Such traders care extra about maximizing their revenue and will likely be much less discriminating about which inventory they promote places on. These individuals do not wish to personal the underlying safety. I like my sleep far an excessive amount of to play brief places on this manner. I’m solely keen to promote places on firms I’m keen to purchase at costs I’m keen to pay. For that motive, being exercised is not the hardship for me that it could be for a lot of different put writers. My recommendation is that in case you are contemplating this technique your self, you’d be sensible to solely ever write places on firms you would be joyful to personal.

In my view, put writers tackle threat, however they tackle much less threat (generally considerably much less threat) than inventory patrons in a important manner. Short put writers generate revenue merely for taking over the duty to purchase a enterprise that they like at a value that they discover enticing. This circumstance is objectively higher than merely taking the prevailing market value. This is why I contemplate the dangers of promoting places on a given day to be far decrease than the dangers related to merely shopping for the inventory on that day.

I’ll conclude this slightly lengthy dialogue of dangers by trying once more on the specifics of the commerce I’m recommending. If Harley Davidson shares stay above $25 over the following twelve months, traders will merely pocket the premium and transfer on. If the shares fall in value, traders will likely be obliged to purchase, however will accomplish that at a value considerably decrease than the present degree. Both outcomes are very acceptable for my part, so I contemplate this commerce to be the definition of “risk reducing.” It’s unusual to finish a dialogue about threat by describing how these scale back threat, however we will’t get round the truth that they do.

Conclusion

In my view, the perfect description I’ve heard of “Harley Culture” comes from a buddy of mine who characterizes it as “try hard boomer cheezy.” That stated, I don’t have to love the product to love the inventory. I believe the dividend is fairly properly lined, and I believe there’s a greater than 50% probability that it’ll be raised again to pre-pandemic ranges over the following few years. Given that it is a money cow, such a transfer would doubtless elevate the inventory value. In addition, I’m a fan of the put choices described above. They provide traders what I contemplate to be a “win-win” commerce. If the shares proceed to drop, the investor will likely be obliged to purchase this dividend payer at an excellent greater yield. If the shares stay above $25… properly, what occurs then. If you’re snug with put choices, I’d suggest the identical or related trades. If you’re not, I’d suggest shopping for a small place within the inventory, and be ready so as to add as value turns into much more enticing within the brief time period. Remember, shiny aspect up, and, in the event you’re a Harley rider, wave again each every so often.