RECVISUAL/iStock through Getty Images

It’s official: buyers’ years-long love for progress shares has taken an enormous breather. So too has buyers’ consolation with small-cap shares. Even although we’ve got seemingly handed the financial valley of the pandemic, the market has continued to flock to large-cap shares on the expense of their smaller counterparts.

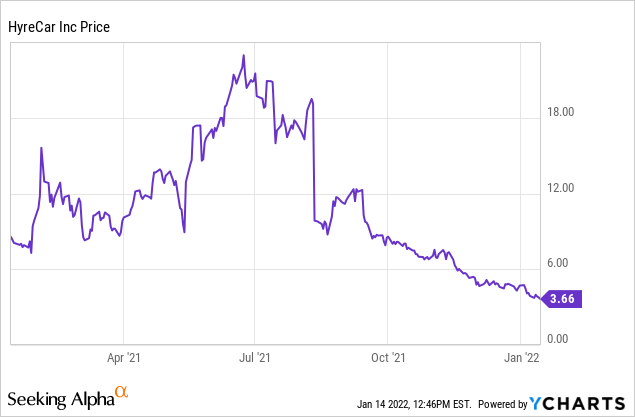

It’s not an enormous marvel, then, that micro-cap HyreCar (HYRE) was left within the mud. HyreCar was a serious progress inventory final 12 months, with its narrative of renting automobiles out to potential Uber (UBER) and Lyft (NASDAQ:LYFT) drivers aligning nicely to buyers’ tastes on the time. Since then, nevertheless, a slower tempo of market growth plus large query marks on profitability, plus the final lack of constructive sentiment for small-cap progress shares, has decimated HyreCar’s inventory. Shares have misplaced ~80% of their peak values within the mid-$20s, and have misplaced about 20% of their worth in 2022 alone.

I will not mince phrases right here: HyreCar is a combined bag of dangers and alternatives. While latest outcomes and commentary from the corporate have definitely opened up the doorway to a bearish case for HyreCar, I’d argue that the corporate’s tiny market cap and its swift fall from heights in almost straight periods since July bears a second probability.

The backside line right here: regardless of the combined messages that we have been getting from the corporate, I believe the dip is price shopping for right into a small rebound play.

The unhealthy information: Insurance and margins

Let’s begin with the damaging information on HyreCar. Last 12 months, the corporate had publicized and dedicated to a goal of hitting adjusted EBITDA profitability by the point it had reached 30k weekly rental days. Well, HyreCar is almost there – it now not reviews weekly rental days, however in its most up-to-date quarter (Q3), quarterly rental days have been 329k, so dividing by 13 weeks provides us a weekly common of 25.2k weekly rental days. However, the corporate remains to be a far methods away from profitability.

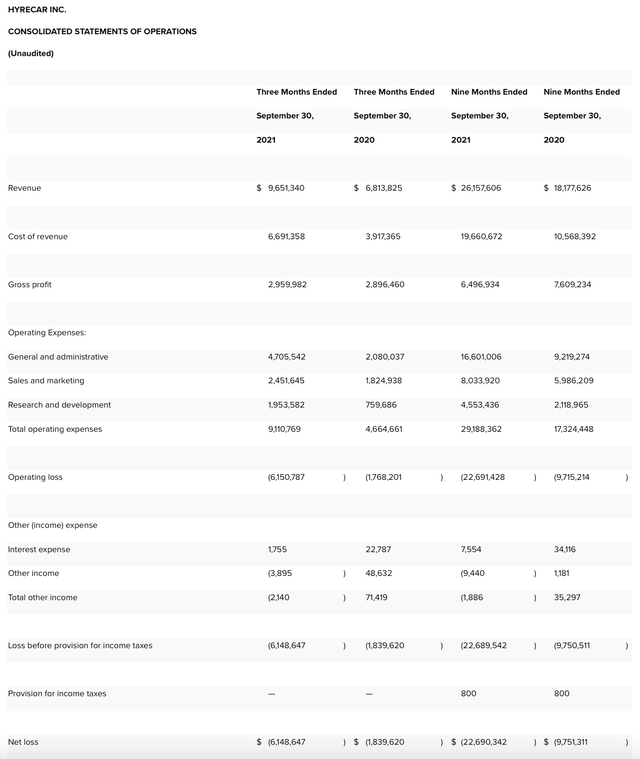

Figure 1. HyreCar Q3 outcomes

HyreCar Q3 outcomes HyreCar Q3 earnings launch

Take a take a look at HyreCar’s Q3 outcomes above. GAAP internet losses widened to -$6.1 million, greater than triple final 12 months’s lack of -$1.8 million. And regardless of 43% y/y income progress in Q3, HyreCar’s gross revenue remained roughly flat at $3.0 million. Gross margin, in the meantime, slipped dramatically to 30.7%, down from 42.5% within the year-ago quarter.

The major driver right here is car insurance coverage prices. Claims have gone up, sending HyreCar’s premiums larger. The excellent news, nevertheless, is that margins are on the rise and anticipated to proceed bettering. Sequentially, the 31% margin this quarter was higher than 24% in Q2, and the corporate is anticipating a mid-30s margin for This fall.

Here’s some commentary relating to margin efficiency from CFO Serge De Bock’s ready remarks on the Q3 earnings name:

We achieved this value discount [versus Q2] by a four-pronged approached. First, we enhance our inside claims processes and insurance policies. Second, we deal with our value management partnering with our exterior new claims processing companion to tailor their course of to HyreCar. Third, we develop the declare’s prescreening course of to scale back general insurance coverage prices. And lastly, we proceed to deal with acceptable threat pricing, charging drivers extra successfully based mostly on their threat profiles. Meanwhile, we maintained our Q2 good points in buyer satisfaction after rolling out these initiatives, balancing threat management and retention of worthwhile drivers […]

Looking ahead to This fall gross revenue margins, we’re on monitor to ship a mid-30s gross margin in This fall with a medium-term aim to surpass 40% within the latter half of 2022 and past. We’ll proceed to refine our pricing and product providing for premium protection plans which we imagine will keep our present ascending trajectory in This fall. And we’re creating new incentives for our drivers with low claims expertise. “

I’ll add one caution here: HyreCar has been known to back down from prior profitability claims. It’s understandable that investors aren’t yet giving HyreCar credit for results it has not delivered yet; however, a veritable return to a mid-30s or low-40s gross margin would go a long way in restoring confidence to this stock.

The good news: robust growth, opportunities for improved supply, and a new Uber deal

In my view, there’s a bevy of good news to counteract the more mixed realities on profitability and margins.

First, on growth – as mentioned in the prior section, HyreCar’s 42% y/y growth in revenue was still quite impressive, and reflecting a large and greenfield market opportunity in which many people want to be freelance rideshare drivers (especially driven by the pandemic), but may not have the cars to do so. Rental days on the platform, also as mentioned previously, grew 20% y/y to 329k for the quarter.

Another major improvement: HyreCar’s take rates, or the amount that it monetizes per rental, has also improved by 7% y/y. The company also expects take rates to continue growing throughout the year, as mentioned by CEO Joe Furnari on the Q3 earnings call:

Take rates have increased significantly as robust driver demand and fewer driver alternatives were creating incremental margin pick-up in our daily rates. Our dynamic pricing model brought take rates up to $29 per day in Q3, up 7% from Q2. Because we’ve invested in building a robust data environment and flexible technology stack, we were able to implement these changes relatively quickly. We anticipate take rate growth through the rest of the year as the dynamic pricing model learns and iterates for risk and reward.”

The firm additionally talked about an expanded partnership with lender Cogent and AmeriDrive to extend the availability of automobiles on HyreCar’s platform. While the AmeriDrive deal has been within the works for a number of quarters, it has had a slower ramp in bettering automobile availability on HyreCar’s platform, which is likely one of the chief impediments towards HyreCar’s growth into different markets.

Another constructive announcement: HyreCar is now an official companion of Uber. Through the settlement, HyreCar now can work instantly with drivers on the Uber platform (for both rideshare or freight drivers) to match them with accessible automobiles. This partnership is getting a gradual rollout, beginning first in main metro areas – however in my opinion, it is an ideal legitimizer for HyreCar’s platform that ought to velocity adoption.

Key takeaways

I believe it is untimely to dismiss HyreCar out of hand, particularly as the corporate’s new settlement with Uber vastly seals the corporate’s popularity. With extra secular tailwinds driving each the rideshare/supply economic system in addition to the need for folks to be freelance contractors, I believe HyreCar is uniquely positioned to proceed rising in its very area of interest market. There could also be near-term operational hiccups, however scale will resolve most of its issues. Stay lengthy right here.